February 2020 Portfolio Review

Total Return: +11.6% YTD (+20.2% vs S&P)

February turned out to be quite shall we say…energetic? The earnings calendar involved roughly 60% of my portfolio – including ~38% on 2/13 alone in the form of AYX, ROKU and DDOG – so I was already on high alert coming into the month. As February progressed the ongoing coronavirus outbreak combined with US election rhetoric to create a very skittish market. That in turn led to some rapid news cycles along with an uptick of traffic on the boards. Finally, the month concluded with additional reports for companies I hold or watch. In the end there was no shortage of info to follow as things played out.

I’m guessing like most here I saw portfolio gains the first 2/3 of the month before the market mixed in some steep declines over the last 10 days or so. We seemed to hit peak market/coronavirus/Twitterverse panic this week. It’s been an epic bloodbath in real time with 1000+ point drops in the Dow, plunging portfolios as far as the eye can see and dire warnings to Sell!, SELL!!, SELLLLLLLL!!!

In fact, reflecting upon my long and storied investment career I hadn’t experienced this past Monday’s brand of single-day carnage in my portfolio since…<*flip, flip, flip, flip*>…February 5, 2020! I realize how hard it is to stay the course while enduring these kinds of once-every-19-days rarities, but this week was a great reminder of the intestinal fortitude needed to stay invested during such turbulent times.

All sarcasm aside 15%+ corrections are never comfortable even when coming off all-time highs, especially over such a short period of time. Fortunately, I’ve somehow found a way to hold on. I hope others have too. In the bigger picture I have no intention of belittling the emotional swings of market ups and downs. And I’m certainly not discounting the dangers or effects of the coronavirus on those people and families who have been affected. However, this week was a glaring example of the avalanche of sound bites bombarding us daily in today’s click-driven, overstimulated world.

It’s important to remember that market corrections are not only normal but healthy. Could this be bigger than that? Heck if I know. I have no doubt someday we’ll turn a corner and find ourselves in a recession. A bear market is undoubtedly around a corner as well. However, acting like impending doom is around every corner is not only exhausting but utterly useless. It’s been proven repeatedly that market timing is not a sustainable plan, so I’m not even going to try. Instead I’ll remind myself for the millionth time to remain focused on the things I can control rather than being distracted by the never-ending cacophony of kneejerk proclamations. And you know what? Each time I remind myself, staying calm gets easier and easier. Let’s not forget I experienced ~30% drawdowns August-December 2018 and again July-September 2019, so it’s not like I haven’t seen this before even in recent times. I not only survived but have actually rebounded to challenge new highs. From an investing standpoint I’m certain my companies aren’t going to self-destruct any time soon. Therefore, neither will I.

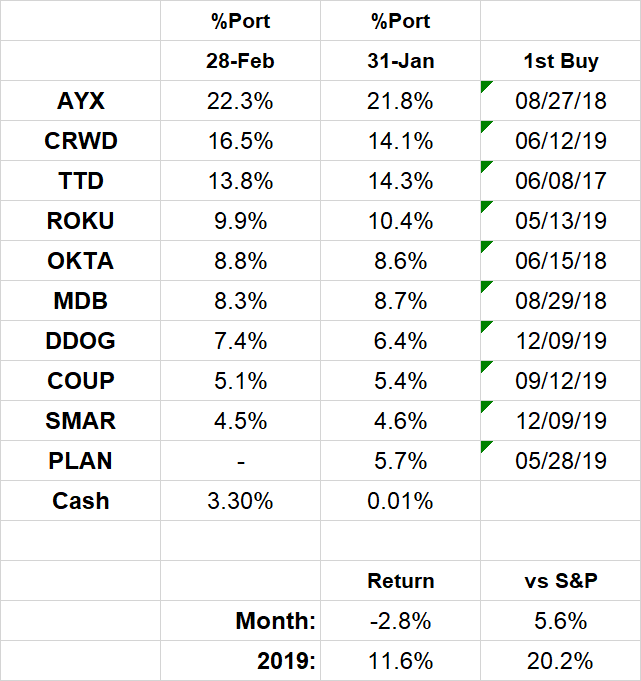

2020 Results:

February Portfolio and Results:

Past recaps for anyone who’s interested:

December 2019 (contains external links to monthlies)

Stock Comments:

I was on track to end February holding the same ten names for the last three recaps. PLAN nixed that possibility just two days short with a disappointing 2/27 report that caused me to sell. Half my portfolio announced earnings this month. The remaining half is spread throughout March. We’ll see where the new info leads. In the meantime, I’ll take the weekend to consider my options and put the rest of my newfound cash back to work next week.

AYX – Being its my #1 position AYX’s 2/13 earnings were highly anticipated. Not surprisingly, Alteryx didn’t disappoint. The company once again crushed estimates on both the top and bottom lines. Their call showed its usual confidence, and the business seems to be firing on all cylinders. I saw some minor hemming and hawing about their guide being too low, but 1) growth has historically slowed from Q4 to Q1 before picking back up and 2) they are serial sandbaggers. I still see them challenging at least 50% next quarter, which would put them right in line with 1Q19 (51%) and 1Q18 (50%). During the call the CFO stated, “Quarterly revenue seasonality will be consistent with what we experienced in 2019.” He said the exact same thing exiting 2018, so I’d anticipate another back loaded year with healthy sequential gains. In the big picture I see no reason why Alteryx won’t continue to be a great company to own in 2020. AYX remains my top conviction holding, and it’s not even close.

COUP – Coupa had a relatively quiet month. I don’t have much to add other than their next report is 3/16.

CRWD – I kicked off February by adding another ~0.4% with my regular monthly contribution. I already had enough AYX and viewed CrowdStrike as my next best idea. I also took advantage of TTD’s February surge to swap ~2% more into CRWD when the latter dropped sharply on 2/20. I’m happy with my current allocation and look forward to earnings on 3/19.

DDOG – Datadog made a huge YTD run into its second report as a public company. Much like its first report, the results were excellent. Revenue growth came in at 84.5% for Q4 and 83.2% for the FY. Total customer growth accelerated sequentially to 37% and the company now has 858 customers with an ARR of at least $100K (+89%). Their new releases are gaining traction, and 60% of current customers are using two or more of their products (vs just 25% last year). Likewise, 65% of new deals are being booked with 2+ products (vs another 25% comp). In aggregate, roughly 1/4 of their clients have deployed offerings from all three business segments: infrastructure, log and APM. That number last year was just 5%. To top it off, DDOG’s already touched profitability with positive operating (6.1%), net (8.9%) and FCF (9.6%) margins in Q4. Management states they are in the early stages of “selling a platform”, and the numbers thus far suggest that is very much the case.

As far as the stock, DDOG experienced a small post-earnings dip and then drifted down before an end-of-month bounce. Given the stellar numbers, it’s hard to chalk up the initial decline to anything other than a combination of selling the news and some high valuation profit taking. There’s no denying DDOG’s pricey, but I’m not sure what else you could ask for as far as business performance. I added ~1% on 2/28 and will likely look to increase this position as we go.

MDB – For what it’s worth, I think Mongo’s had a sneaky effective 2020. With much less fanfare than many names we discuss, MDB has somehow found a way to rise 16% YTD in a terrible market. The decrease in Mongo’s revenue growth the last couple quarters has been much discussed here, but the stock seems to have been resilient thus far. Mongo will finally tell us exactly how tough those tough Q4 comps are when they report on 3/17. Fingers crossed for those who hold it. 🤞

OKTA – Earnings 3/5. No news is good news?

PLAN – Well, that smarted. Anaplan had been a profitable secondary holding with a spot in my portfolio 12 of the past 13 months. That all came crashing down with their 2/27 report. I thought the baseline numbers were reasonable, and the company actually raised the FY21 pre-estimate they gave after Q3. The flipside is this quarter’s beat was their smallest ever with a guide that implies a continued slowdown even if they outperform next quarter. To make matters worse, they also posted sharp declines in billings and deferred revenue while announcing their Chief Growth Officer would be leaving. There’s been a recent run of companies reporting billings slowdowns in conjunction with some sort of adjustment to whatever Growth or Revenue executive is responsible for that area. Most have been punished by the market, and PLAN was no exception. I thought the pre-market plunge was a bit overdone, but with everything else being on sale I decided to sell my shares to repurpose the funds. Plugging everything in, I ended up selling a position up 32.3% at the 2/26 close for a 2.8% loss at the 2/27 open. I believe the French refer to events like this with the phrase “c’est la vie”. Where I grew up in South Jersey we preferred “%&#@!$^”!!!!!

ROKU – And the volatility continues. After being my only market-trailing stock in January, Roku charged out of the February gate. It surged right away when Roku settled its Fox dispute and then continued to climb into mid-month. While the Fox agreement was certainly a welcome (and anticipated) development, I viewed it as nothing more than a prelude to a pretty significant earnings report on 2/13. The company spent most of 2019 very aggressively expanding its viewing platform and OS footprint. This report would shed some initial light on just how well those efforts had positioned the company for 2020 and beyond.

I personally thought things looked pretty good. Roku posted 49.1% total revenue growth with its higher-margin platform growth coming in at 71.5%. For FY19 those rates finished at 52.0% and 77.7%, respectively. Active accounts (+36%), streaming hours (+60%) and average revenue per user (+29%) all continue to grow at strong rates. Platform as a percentage of revenues has increased from 43.9% to 56.1% to 65.6% the last 3 years and is expected to be ~75% for 2020. Roku not only ended 2019 with its OS in roughly 1/3 of US smart TV purchases but also laid the groundwork for additional expansion into North America, Europe and Brazil. The call was confident, and I didn’t sense any unanticipated headwinds on the horizon. Finally, Roku’s top-end 50% Q1 revenue guide would mean sequential acceleration, and even a moderate beat would also be YoY acceleration vs 1Q19’s 51.3%. Accelerating 50%+ growth coming off a $1.13B revenue year? Sounds good to me.

Unfortunately, the market didn’t share my enthusiasm for very long. The stock initially spiked up ~8% at the open (*wistful sigh*) before crashing down to finish the day at -6.5%. And Roku’s been stuck in the mud ever since. The decline was apparently spurred by analyst concerns about the below consensus FY20 guide for breakeven EBITDA and GAAP losses, due mostly to integration of the dataxu acquisition. As a reminder, this is the very same EBITDA guide they made for most of FY19 before finishing at +$36M. Management has been very explicit about their growth intentions, and the returns have been positive so far. They state they are “well positioned for the new streaming decade”, and I can’t really argue that point. Given the guide and underlying metrics, it’s not hard for me to picture strong revenues and positive EBITDA in 2020…

…but what I see is only part of the puzzle. Despite believing Roku has an excellent plan, I must admit disappointment in the post-earnings action. The early month climb and initial earnings pop made sense to me (ownership bias maybe?). The subsequent action has not. That’s led to a bit of a gut check. While Roku’s been a profitable buy, I can’t ignore most of my position has basically been dead money for six months while trailing the market significantly. At some point that means something. Not because I’ve soured on the business, but because holding such a condensed number of stocks really highlights the effect of opportunity cost for any “wait it out” portion of your portfolio. I’m all for Roku’s continued expansion, and in theory their shift to maximizing platform revenues and ARPU should have some coiled spring effect once it kicks in. It obviously didn’t with this quarter’s earnings, so the challenge becomes determining the acceptable hold time and allocation for a stock that might stagnate further while I await signs of the payoff.

Being brutally honest with myself, I’ve previously found ways to trust NTNX, SQ, TWLO and ESTC’s numbers a little too long even though the market was telling me otherwise. Simply put, I don’t need to fight city hall when there are other options available. After all, I’m not here to prove the market wrong. My only goal is maximizing returns. Given that, I’m beginning to question how committed I am to ~10% of my portfolio potentially drifting for another quarter at least. I can’t see myself abandoning Roku since I still like the business very much, but it does enter March as a candidate for a lower allocation depending on my remaining earnings results.

SHOP – < No comments. Just quietly nodding my head admiringly. >

SMAR – I’ve stayed disciplined to my December process for selecting Smartsheet to round out my portfolio despite the fact it was Zoom I passed over to make the choice. SMAR’s numbers are strong enough to deserve its spot. Nevertheless, the company will need to prove it’s maintaining that level of performance when it reports 3/17. Otherwise, the top of my watch list is nipping very closely at its heels...

TTD – The Trade Desk just kept on truckin’ to start February. It was my best performer through the first three weeks and climbed back above 15% of my portfolio as a result. I decided to take advantage of the spurt by swapping ~2% into more CRWD when the latter plummeted on 2/20. That cut my TTD allocation to ~13.5%, which was a level I was more comfortable with heading into 2/27 earnings. Despite having no doubts Jeff Green would sell the crap out of 2020, I wanted a touch less exposure while waiting to see if the numbers backed up the narrative.

The early returns suggest TTD is still positioned to keep delivering. They not only beat both the top and bottom lines but more importantly guided for reaccelerating revenue growth next quarter. CTV spend rose 137% for the year, and they anticipate another doubling in FY20. Profitability continues to impress with net margins (26.7%) accelerating for the third year in a row and EBITDA margin (32.4%) topping 30% for the fourth consecutive year. TTD enters 2020 guiding toward that 30% EBITDA mark for the first time, which makes it possible if not probable TTD posts accelerating FY20 profits even as the company continues to invest in growth. If nothing else, it does appear the ad market continues to move rapidly toward a data-driven and programmatic approach. That part of the narrative remains very much intact, and the 15% pop on a brutal market day seems to back that sentiment. Consequently, I see no reason not to continue riding the TTD wave.

ZM - < No comments. Just quietly nodding my head even more admiringly. >

My current watch list in rough order is ZM, NET, DOCU, LVGO, SHOP, WORK and PAYC. Further back on the radar are TWLO, ZEN, EVBG and AVLR. Avalara fell to my secondary list after its 2/12 release suggested a growth slowdown in what I had already thought might be a niche market. While it’s an interesting business, I believe there are better growth/TAM combos to consider at present. Fastly’s 2/20 release didn’t do much to change my prior ambivalence. I thought the numbers were just OK, and they announced a major management shuffle in conjunction with earnings. I’m a pass for now.

Bill.com gets its own special category since I’m not sure where it fits just yet. BILL is intriguing, but I’ll probably wait at least another quarter to better understand the business and underlying revenue splits. They broke out three income streams on their first call as a public company: subscriptions, transactions and float interest. Unfortunately, their S1 history isn’t as specific (that I could find) so the individual trends are hard to gauge. Given its meteoric rise since IPO and the fact the overall numbers aren’t THAT dynamic compared to some others, I’m content to keep it a watch for now.

Finally, I’ve just started digging on ENPH after yet another excellent quarter but have nothing to say yet except the numbers are super impressive.

And there you have it. As outlined above, February was quite exciting. In fact, I can’t remember an odder month. Despite ending on a very sour note, I experienced some amazing positives. My portfolio rocketed 6.4% out of the chute, immediately plummeted 5.2% on 2/5 alone, shot back up to briefly pass my all-time high midday on 2/13, then closed at a new ATH on Valentine’s Day. I must admit that was a much better (and less fattening) gift than chocolates.

I wrote last month of needing an 8.51% gain to reclaim my personal high-water mark. Little did I know it would take only 8.5 trading days for that to happen. The 2/14 ATH put my entire portfolio up 92.8% since 1/1/19. It touched 93.8% (25.3% YTD) on 2/19 before ending the month at 72.6% (11.6% YTD). Despite the late-month crater, those are still stunning numbers when I think about them.

Investors reference volatility all the time. Fortunately, my volatility has been to the upside more than down in recent months. These companies continue to perform, and the market continues to reward that performance for those taking the longer view. The best part is there are likely more positives to come for many of these names.

Thanks for reading. I’ll gladly take any feedback and I hope everyone has a great March.