April 2020 Portfolio Review

Total Return: +7.8% YTD (+17.7% vs S&P)

What a weird month. Main Street got crushed while Wall Street threw a party. As huge swaths of global commerce evaporated the last few weeks, governments and central banks have gone into hyperdrive propping up cratering economies. All that macro promiscuity appears to have found its mark because markets have swooned in response. Seemingly overnight investors went from victims in a zombie apocalypse…

…to squealing teenagers during Beatlemania.

As a result, the fastest crash in history has now been answered by an equally historic rebound. All in all, it has been a dizzying turn of events.

As we close an April that’s been mostly market-centric, May should turn the spotlight back toward my individual stocks. That’s fine by me since I am much more interested in my companies’ performance than macroeconomic interplay. Current holdings AYX, DDOG, LVGO and ROKU all release earnings within the next two weeks. Watch listers ESTC, EVBG, FSLY, NET, SHOP, TWLO, TTD and ZS either will or should report in May as well. I view this upcoming earnings season as a moment of truth for the SaaS business model. We are about to find out just how reliable recurring revenues and net expansion rates are for supporting growth in leaner times. We should also gain considerable insight into just how mission critical some of these products might be. It is unfortunate the initial stress test is under such extreme economic circumstances, but it is what it is. From that perspective May should be fascinating.

So, buckle up buttercup…

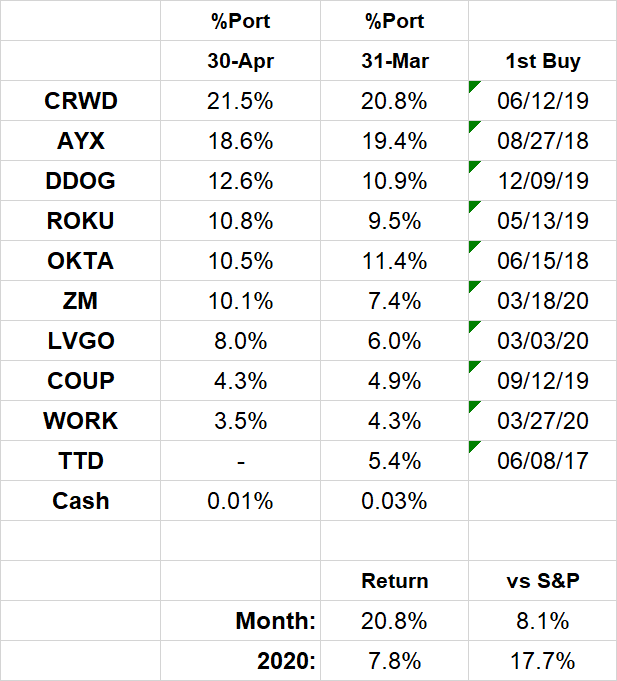

2020 Results:

April Portfolio and Results:

2020 Monthly Allocations:

Key:

darker green - started during month

lighter green - added during month

yellow - trimmed during month

blue - bought and sold during month

red - position exits

Past recaps:

December 2019 (contains external links to 2019 monthlies)

Stock Comments:

After a very active March this month was remarkably tame. On 4/1 I split my small regular contribution into equal nibbles at AYX, CRWD and OKTA. I also partially exited TTD that day before dumping the rest into ZM when Zoom cratered on 4/2. Lastly, I swapped some COUP for LVGO when Livongo preannounced a revenue beat on 4/7. And that was that. Was it strange to do so little with all this extra time to sit around and stare at my portfolio? Kinda, but with no earnings reports there wasn’t much else to do. Trading’s not my thing, and I’ve learned that action for the sake of action mostly loses me money. Just because the world is a little chaotic right now doesn’t mean I should forget that doing nothing can often be the correct choice.

Instead, I ended up doing quite a bit of research on topics I’d like to improve upon such as stock selection and portfolio management. I also discovered a knowledgeable group of Twitter posters holding similar investment philosophies. In retrospect this month was a welcome breather and I believe I’m better for it. I fully expect things to pick back up as May earnings season gets into full swing.

AYX – The market doesn’t quite know what to do with Alteryx lately. After pummeling the stock in March for no apparent reason, that same unseen hand yanked it back up in April. That hand should become much more visible when AYX reports May 6. The main question seems to be just how much the lack of a true cloud offering has affected Alteryx’s sales and usage during this pandemic. We’re about to find out.

COUP – For the second consecutive month I swapped some COUP into LVGO. And for the second consecutive month it wasn’t any dislike of Coupa as much as liking Livongo’s 2020 prospects better. I believe COUP’s platform will serve its clients extremely well during the upcoming months. However, as with most firms there’s uncertainty how much Coupa can grow its business during this lull. I’m willing to downsize my position while waiting to find out.

CRWD – And CrowdStrike cruises right along. The company’s excellent March report and very positive outlook led to a 21.5% April gain. I view CRWD’s business as the strongest in my portfolio right now and see no reason not to sit tight with it as my #1 holding for the second month in a row.

DDOG – Datadog’s 25.4% April was even better than CrowdStrike’s. DDOG’s 2/13 report was outstanding but came far enough before peak virus they were not as specific as some others in addressing the effects of COVID-19 on their business. It is not entirely clear how monitoring firms are going to be affected, but DDOG’s fundamentals should provide excellent support as things shake out. We will get a lot more clarity when DDOG reports on 5/11.

LVGO – Livongo crushed it this month. The stock rose 40.2% as three significant pieces of news hit the wires. The first was Kaiser Permanente offering LVGO’s myStrength app free of charge to all its members. Livongo’s behavioral health offering, myStrength is designed to support mental and emotional health in patients with chronic conditions. Kaiser is a major player in health care, so I view this partnership as another nice win for Livongo.

The second was an article outlining FDA emergency approval for Livongo’s remote blood glucose monitors in hospitals. This action allows healthcare workers who are already rationing personal protection equipment to monitor blood glucose levels of infected COVID-19 patients without being physically present. While the move was clearly necessitated by the virus, it is not hard to see this use case and other forms of remote monitoring being more prevalent even after the pandemic passes. That bodes well for companies like LVGO. Barron’s seems to agree.

Finally, Livongo put out its own release preannouncing first quarter revenue above its initial guide. LVGO now expects $65.5-$66.5M versus $60-$62M. The high end of the new guide would put revenue growth at 107.4% YoY. Management also referenced a record 620 client launches in the quarter and member enrollment that is running ahead of expectations. For context, Livongo launched 231 clients in 1Q19 which means 168% YoY growth in that metric alone. Management did not comment on its previous -$4.5M EBITDA guide, which would be a -6.8% EBITDA margin at $66.5M revenue. I would anticipate this number coming in a bit better as well, though I won’t hold it against LVGO if some of the revenue beat is pushed toward growth initiatives instead. Regardless, EBITDA should end up significantly better than last year’s -$9.2M and -28.6% margin. I was impressed enough to add a few more shares immediately after the news. The official release is May 6. Needless to say, I’m looking forward to it.

OKTA – Okta became my first company to make a public statement on the business effects of COVID-19. Management reaffirmed revenue guidance for the upcoming quarter and year but also commented that billings could see downward pressure. That makes sense. From a revenue perspective, current customers aren’t likely to go anywhere and might even expand usage with so many newly remote workers. However, future billings could get squeezed if potential clients understandably hesitate to commit to new deals. Okta also calls for narrower losses this quarter and year, mostly due to decreased operational and travel expenses. Some of these savings came from their Oktane20 customer event being held virtually rather than live. Considering the circumstances, I view this as encouraging news and a testament to the strength of Okta’s underlying business.

PAYC – Paycom is a former holding and current watch list name I briefly owned again in March. I’m mentioning it again because PAYC reported on 4/28. I had the date circled because I viewed it as my first real peek into how a SaaS company I knew well was being affected by COVID-19. I had two main questions:

1) how well would PAYC’s platform – which I view as mission critical – hold up given the number of small businesses clients using it, and

2) how would management handle guidance?

In this case Paycom posted steady results with only a minor dip in their main performance trends. Revenue came in a hair above the top end guide, and PAYC continues to churn out its usual strong profits and margins. As with most firms reporting recently, management withdrew future guidance given the COVID-19 uncertainty. They did mention future revenue could see temporary pressure from clients reducing headcount since much of PAYC’s pricing is per-employee. However, management sounded confident the fundamental structure of their business model remains sound. The market liked the news enough to shoot the stock up ~15% the next day. Hopefully, this bodes well for the rest of the SaaS companies reporting over the next few weeks.

ROKU – Well, it’s not like I haven’t said on occasion that Roku is volatile. Roku soared as much at 47% this month before finishing at +38.6%. Unfortunately, that shows just how rocky Roku’s 2020 has been since even that gain still leaves it down 9.5% YTD. There were two big pieces of news this month which elevated the stock. The first was the continuation of the company’s UK expansion with the British release of The Roku Channel. As in the US, the channel is free for viewers and supported by ads. The UK version features “10,000+ free movies, TV episodes and documentaries [including] a selection of popular global and British TV series” geared toward local audiences. I’m speculating a bit, but Roku must have projected enough British viewers and more importantly enough advertiser interest to proceed with the launch. I view that as good news.

The second update was a positive preannouncement of Q1 results. I view that as even better news. The highlight was a raise in revenue guidance suggesting this quarter’s growth could end up around 54%. That would mean an acceleration both sequentially and year-over-year, which is very impressive at this scale. The company also estimates increases to 39.8 million accounts and 13.2 billion hours streamed. The kicker was this quote regarding COVID-19:

…beginning in late Q1 Roku started to see the effects of large numbers of people ‘sheltering at home’. For Roku, this has resulted in an acceleration in new account growth and an increase in viewing.

While the underlying circumstances are terribly unfortunate, these developments underscore the popularity of Roku’s platform and have not surprisingly led to a healthy uptick for the stock.

The new numbers lend some credence to my belief COVID-19’s lockdown will only accelerate the move to digital media. Maybe I’m just stubborn, but I have continued to hold my shares despite Roku’s mediocre YTD. My thesis is ad dollars should eventually go where the eyes are and right now the eyes are on streaming. Roku’s platform also gives it optionality TTD lacks while waiting for virus-affected ad budgets to recalibrate. Along those lines, CEO Anthony Wood stated,

We have been working closely with advertisers to help update their plans to reflect new viewing patterns and adjust their overall marketing mix which has been affected by social distancing. While we expect some marketers to pause or reduce ad investments in the near term, we believe that the targeted and measurable TV ads and unique sponsorship capabilities that Roku offers are highly beneficial to brands today.

When it is all said and done, Roku appears to be in a great position to withstand the temporary decline in ad spending and come out stronger on the other side. I’ll get to dig deeper into that theory when Roku formally reports May 7. I stated last month I thought even mildly optimistic news could portend a rebound in the stock. To that end the preannouncement has worked out swimmingly so far. Nonetheless, I’ll have my fine-toothed comb ready for whatever additional info Roku releases.

TTD – This is a slightly bittersweet update. I made my first purchase of The Trade Desk in June 2017. After a stellar 2019 it finished as my #2 holding with a 17.6% allocation. That was a bit too big for my liking, so I’d spent the early part of 2020 slowly trimming the position. I originally intended to stop around 10%, but the coronavirus forced a serious change of plans. Global ad spending has seen some serious shrinkage…

…and TTD’s been pressured as a result. Having already cut it significantly in March, I sold the last of my shares right at the beginning of April. I swapped ~1.5% into Datadog and ~0.3% into Livongo on April 1. The remaining ~3.5% went toward Zoom when the latter cratered the very next day. Google’s recent report suggests ad spending might not be as bad as initially feared, but I still see too much uncertainty the next couple quarters to feel comfortable holding TTD above my other options. Despite its awesome rebound this month, TTD’s already declining growth and the postponement of their expected Olympic revenue has me waiting until CEO Jeff Green’s next earnings sermon to reassess.

My first thought upon exiting was I’ll miss TTD because it was a very profitable buy and one of my favorite stocks to own. My second thought was most successful investors probably don’t miss any position they decide to exit, so I guess I still have some work to do.

WORK – A bit of a head scratcher. I still support the thesis that led me into Slack last month but admit the recent stock performance is puzzling. While other work from home companies had very healthy months, WORK basically remained flat. The market doesn’t quite seem to be on board yet, but I can’t see how Slack isn’t seeing much greater adoption and usage in the current environment. The external narrative seems to back that up even if the stock doesn’t reflect it yet. At this point I remain willing to hold my small position while I await more clarity. I’d gladly take thoughts from others who either hold or have considered WORK.

ZM – An amazing month in all kinds of ways. Zoom went from societal savior to security scourge and back again in about 30 days. As the world moves to Zoom in remarkable numbers, increased traffic and new use cases not surprisingly revealed some technical flaws and security issues. The topic has been parsed to death in just about every outlet imaginable, and the company very openly promised fixes as a result. Zoom has responded quickly so far, including this initial message by founder and CEO Eric Yuan. In it Yuan promised virtually all Zoom’s resources would be focused on security for the next 90 days, and the company has provided regular updates since. They have also enlisted individuals and consultants (including CRWD!) to evaluate their protocols. There is still plenty of work to be done, but Zoom is clearly making the effort. As they very much should considering the potential reward.

The other recent news was Facebook entering the space with a free video chat offering for up to 50 people. Not to be outdone Google just announced something similar with a free version of its Meet offering, although their rollout will likely take a few weeks. How much of a threat does all this pose to Zoom? It is hard to tell. Once thing I noticed though was a lot of people who dismissed Zoom with “yeah, but all these new users are free and they’ll never monetize them” suddenly shouted “OMG!!! FACEBOOK IS TOTALLY GOING TO STEAL ALL OF ZOOM’S FREE USERS!”. My oh-so-hot take is you can’t have it both ways.

The truth is Zoom is experiencing literally unprecedented customer growth and no one knows how things will turn out. That’s what makes a market. One thing I’m fairly comfortable saying is FB presents little to no threat to Zoom’s enterprise business, which let’s not forget is how ZM built its amazing business in the first place. If a customer is concerned about Zoom’s security, are they really going to entrust their privacy to Facebook instead?!? I seriously doubt it. Facebook might be better positioned to monetize free users given their huge advantage in ad-based models, but I don’t view that as the end of the world. Given advertising is well outside Zoom’s circle of competence, I’m not sure that route is in their best interest anyway. The Google announcement is a little different in that Meet has an enterprise offering, but it is still clearly playing catch up to Zoom. After all, Google’s been in this market since its release of Hangouts in 2013 and Meet in 2017. The fact Meet’s free version is being rolled out gradually suggests (to me anyway) Google might be rushing a bit and trying to figure it out as they go.

My main takeaway from all this is Zoom is definitely onto something, so I’m not surprised other companies are showing interest. In fact, it seems just about any firm with a videoconferencing offering is shouting it from the rooftops these days. Some of the recent rush to video will almost certainly stick post-virus, and all this jockeying for position suggests it could be a very lucrative market. Will Zoom stay ahead of the competition? I have no idea, but for now I’ve chosen to put my money on the company in the driver’s seat.

If you sit back and think about it, Zoom has a chance to become a truly iconic global brand faster than any company in history. “Zooming” is now a thing the world over. The company’s exposure has grown to such an extent it’s now earned a spot in the Nasdaq 100. This is an incredible opportunity, and I bumped my position this month as a result. I am looking forward to seeing where this ride takes me.

My current watch list…

…in rough order is NET, DOCU, SHOP, TTD and SMAR. Second tier is TWLO, ZEN, MDB, AVLR, FSLY and EVBG. BILL remains more on the curiosity list at least until next earnings.

And there you have it.

I’m not exactly sure how to feel about April. During a period dominated by generally awful news, I posted one of the best months I’ve ever had in over a quarter century of investing. The silver lining is the market is always forward looking, so at least optimism seems to rule the day. Here’s hoping the market is right in that regard.

This month’s performance – led by LVGO (40.2%), COUP (26.0%), DDOG (25.4%) and the Dr. Jekyll version of ROKU (38.6%) – has now shoved me back into the green for 2020. That is a welcome development after PLAN, TTD and the Mr. Hyde version of ROKU put a huge dent in my February and March returns. While my performance isn’t quite as strong as some others I follow, I’m satisfied given the circumstances. I’m also pleased with my focus this month after what I felt was a wobbly March. Sitting tight and paying attention did wonders. It also helped that a few of my companies provided useful updates along the way. As mentioned earlier, even more clarity should be on the way as earnings reports ramp up this week. Rest assured I’ll be paying close attention.

Thanks for reading and please continue to do the right things to keep everyone safe and healthy. Until next time, I hope everyone has a great May.

Good write up, but I still not sure about “ live longer” XD, IMO there’s too many blind spots to window dressing the enhanced number to convince enterprises to got the EVA. I know they seems like got some proof from FDA(? Not totally sure). I rather wait for more time to understand the field that I’m not familiar. Another thing is TTD, LOL I really want see the numbers next Q.

Thanks for your thoughts and wish all have a great earning month!