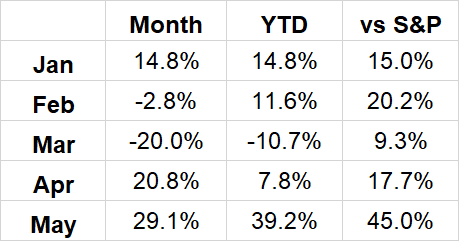

May 2020 Portfolio Review

Total Return: +39.2% YTD (+45.0% vs S&P)

Mr. Market’s Minions: “Sell in May and go away!”

Me: “Nah, I’m good.”

Well, that was…interesting. After an excellent April, May kicked off with ~50% of my portfolio reporting earnings over the first 11 days. I viewed this stretch as a major test for the SaaS business model. We were about to get our first look at just how sturdy recurring revenues and net expansion rates would be during a sharp economic downturn. I’m glad to say those metrics seem to have held up just fine for those companies whose products have proven to be mission-critical for customer success. In fact, there is a legitimate argument business software has never been as important as it is in today’s newly remote workplace.

The world is clearly undergoing massive upheaval, and most global industry has been disrupted right along with it. Employers and employees are both scrambling to adjust. Several companies reporting this month noted a sharp business decline in March before seeing things start to stabilize in April. Likewise, many analysts and investors are focusing not only on current operations but also on post-COVID expectations. That’s not surprising given the forward-looking nature of the market. Companies appearing well-positioned to navigate these changes are presently getting a lot of love from the market. Sadly, those looking like they might lag behind are quickly being taken to the woodshed. I’m fortunate most of my companies have fallen into the former category thus far.

I enter June with the remainder of my companies all reporting earnings between 6/2 and 6/8. While I have no idea what their numbers will be, I do find some comfort in the fact similar businesses seem to be weathering this storm amazingly well. Here’s hoping at least a little of April and May’s crazy rebound continues to carry over.

Fingers crossed. 🤞

2020 Results:

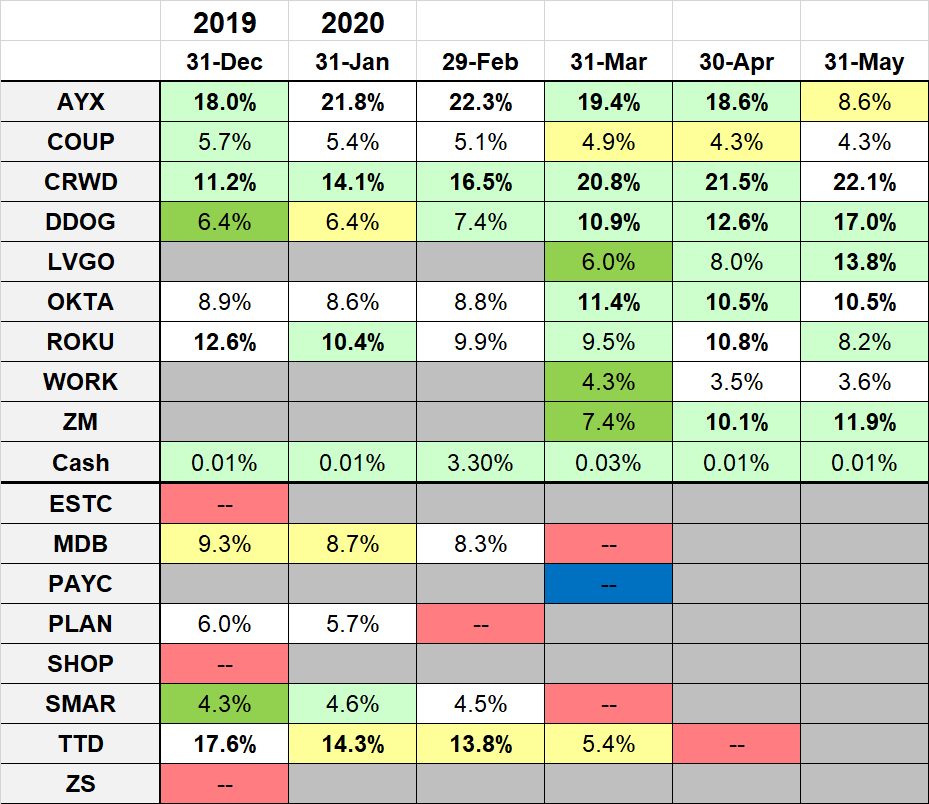

May Portfolio and Results:

2020 Monthly Allocations:

Key:

darker green - started during month

lighter green - added during month

yellow - trimmed during month

blue - bought and sold during month

red - position exits

Past recaps:

December 2019 (contains external links to all 2019 monthly reports)

Stock Comments:

I end May holding the same names for the third consecutive month. However, I significantly trimmed AYX after earnings to free up ~10% cash. I always prefer being fully invested, but in trying to stay disciplined it took a couple of weeks to filter that much cash back into my portfolio. While I considered several watch listers during the shuffle, I ended up adding to DDOG, LVGO and ZM instead.

AYX – Alteryx had a much-awaited earnings release on 5/6. As with most firms reporting in May there was considerable speculation about the effects of COVID-19 on its business. Most of the concern centered around Alteryx’s position as more of an on-prem product than true cloud offering. While no one doubts the inevitability of data analytics, there was legitimate uncertainty regarding how well AYX’s products would translate in the remote work world.

It turns out Alteryx isn’t immune to COVID-19. Revenues came in at $108.8M and 43.2% growth. Despite being at the top of the guided range, that is by far the smallest growth AYX has posted in the 15 quarters of data I have on the company. It was also their smallest beat by a significant margin in both dollar amount ($0.83M) and percentage terms (0.8%). For a company with a reputation as serial sandbaggers on guidance, it was hard to call this anything but a mild disappointment.

The secondary numbers weren’t terrible but also not what we’re used to. In fact, I’d call it a mixed bag. On one hand, AYX generated $20M in operating cash flow and posted its usual incredible 91% gross margins. On the other, the company saw “an abrupt and significant change in customer buying behavior in March”, particularly “opportunities with new customers and expansion opportunities that were not attached to a renewal”. US business actually appeared to hold up pretty well (+52% YoY). Unfortunately, international revenue took a hit with only 22% YoY growth for 26% of total revenues vs 54% growth and 30% of total revenue in 1Q19. Management noted this difference on the call and implied most of the drop was due to a slowdown in Europe.

The overall decline unfortunately found the bottom line as well. AYX posted its first operating and net losses in 11 quarters. Management mentioned delayed sales, and the 128% NER is the first below 130% in 14 quarters. Operating expenses saw some pressure even when considering one-time charges, though the CFO was quick to point out expenses should get back in line for Q2. Hiring has been paused, nonessential spending has been cut and user conferences have been pushed from 2020 to 2021. While there is nothing fatal in any of this, it’s apparent a company that had been roaring full throttle for several quarters is now judiciously tapping the brakes as it surveys the road ahead.

When the press release numbers support my thesis, I usually prefer to wait for the transcript rather than listen to the call. In this case, I had no choice but to settle in to hear what CEO Dean Stoecker and friends had to say. Management continues to have great confidence in their business – which they should, frankly – but it is also apparent AYX is adopting a much more conservative approach to COVID-19 than most of my other holdings. Instead of demonstrating its clear value add in this environment like say ZM or CRWD, Alteryx seems unsure exactly how it fits in the new remote worker dynamic. Yes, the long-term trend toward analytics will undoubtedly roll on. Alas, it appears AYX will face some temporary headwinds as long as COVID-19 restrictions remain in place. Or as the CFO put it, “The current macroeconomic environment is clearly in a state of turmoil, and we expect it will continue to negatively impact our business.” As a result, AYX guides for just 15% top end revenue growth next quarter and a top end operating loss of -$9M (-9.5% margin). Like most firms it has also withdrawn its FY number. Yet no matter how many times Stoecker says “conservative” when pressed on the guide, 15% is 15% even when you sandbag. Alteryx has plenty of cash flow and money on hand, so survivability is not a concern. However, this quarter makes it clear AYX is more susceptible to the present macro conditions than I had thought and hoped.

As outlined earlier, much of Alteryx’s slowdown this quarter seemed to originate with its European business. I can’t help but note COVID-19 hit Europe about a month before coming to America. Does the fact the US has lagged many countries in overcoming the virus account for some of management’s hesitancy? It sounds like April stabilized, but how should we weight risk for May or June if this drags on longer than anticipated? Those are valid inquiries – at least in my mind – considering the US accounts for 70%+ of AYX’s business. I’m not smart enough to answer these questions, and my crystal ball has never served as anything more than a murky paperweight. As a result, I have no choice but to adjust my immediate conviction on the stock.

Alteryx entered May as my #2 position after being at or near my top spot for over a year. It has been an excellent investment, and I remain a huge fan of the company’s future. Data analytics isn’t going anywhere, and even as this slowdown plays out AYX has announced a new end-to-end platform for automating analytic processes. Management is very confident in this new offering and views it as a category they “intend to own”. Despite the minor virus-related revenue hiccup, Alteryx continues to position itself for major long-term success.

Still, the surprising numbers and uncertain landscape have put me in a much different headspace regarding allocation size. Therefore, I ended up trimming ~60% of my shares. It’s not a belief-in-the-company issue. It’s strictly a matter of personal risk in an uncertain time. I have zero issue with a smart, proven management team deciding to hunker down for a spell. The tradeoff is there’s zero chance I am hunkerin’ down alongside with 18%+ of my portfolio. I’m much more comfortable with 8%-10% as things work themselves out. If I end up missing out a bit in the short term, c’est la vie. DDOG and LVGO have passed AYX on my present conviction meter, so that’s where the majority of funds ended up. A portion found its way into ZM as well later in the month.

COUP – A boring good +29.2% month for a boring good stock. The efficiency of Coupa’s platform has almost certainly been invaluable to its users these last few months. The question is just how much new business COUP will land given the likelihood many potential customers are currently tightening their belts. I’m guessing customer growth will be a main focus when earnings are released on 6/8.

CRWD – CrowdStrike continues to hold down my #1 spot. Last quarter was a total blowout, and management’s comments at the time suggested much of that incredible performance could carry over to this one as well. We will find out whether that is indeed the case when CRWD reports after the bell on 6/2.

DDOG – Datadog proved its bite is every bit as big as its bark by crushing its 5/11 earnings report. My first comment is more an impression on the corporate culture than the business. CEO Olivier Pomel initiated the call by noting all employees received a grant to support productivity and safety when forced to work from home. At their discretion employees could donate all or a portion to charities that help with COVID relief if they so desired. Pomel stated the program has resulted in $1M worth of employee donations so far. That’s pretty cool.

As far as the report itself, I am not sure what else you could ask for as a shareholder. The $131.3M in revenue and 87.4% YoY growth trounced expectations. Gross profit growth was even better, coming in at 105% (!!!) vs 92% last quarter and 67% in 1Q19. They easily set margin records for gross (80.2%), operating (12.3%), net (14.3%) and FCF (14.7%). Net expansion finished at 130%+ for the 11th consecutive quarter. DDOG is killing it, and like many SaaS firms notes long-term trends “may even be accelerated or amplified”. The frictionless, bottom up sales model they continually tout really paid off this quarter. With no professional services or hands-on-keyboard implementation needed, they saw “limited impact from COVID” in their ability to onboard new business.

Breaking down their products, it appears almost everything is selling like hotcakes. This quarter saw 63% of customers using 2+ products, up from 58% last quarter and 32% last year. In addition, approximately 75% of new logos landed in the 2+ category, meaning this number is likely to grow even further. Management noted several times they are seeing hyper growth across their entire product line rather than just one specific area. Management intends on “investing across the board and believe we are well-positioned to execute on our plans for growth.” The enthusiasm was palpable on their call, which is perfectly understanding given the excellent results.

No matter how you slice it, DDOG’s future looks very bright. Even adjusting for COVID uncertainty and possible “deal slippage”, the company felt comfortable guiding for 63% top end growth next quarter and raising their FY top end to $565M (+56%). They also project positive operating income and EPS for the year. That’s an amazing timeline for a firm still just eight months from its IPO. The company took advantage of its recent success to announce a private offering of $650M in convertible notes to further fund what has been some very impressive growth. When you break it down, the stock’s recent run appears very justified.

As far as my holdings, I was able to add ~1% more immediately following the earnings release before the price got away from me after hours. No big deal though. I added another 1% on the big pullback a couple days later. As we exit the month, I’m happy with my allocation and ecstatic about the business. I’d anticipate DDOG remaining a top holding for the foreseeable future.

LVGO – Livongo remains on fire. The company’s positive late-April earnings preannouncement led to a very nice run into its 5/6 report. While this sometimes leads to the market selling the news, LVGO’s main course turned out to be even better than the appetizer. Revenue of $68.8M beat the adjusted top end $66.5M guide for an impressive 115% YoY growth rate. Gross profits grew 127%, estimated agreement value increased 85% and enrollment for their core diabetes offering grew 100% to 328,510 members. Livongo launched a record number of clients in the quarter and now has 1,252 overall (+77% YoY). Even as management “continues to closely monitor the situation relating to the COVID-19 pandemic”, they felt comfortable enough to raise top end FY guidance from $290M to $303M. Business appears to be booming.

What makes it even better is it’s not just sexy headline numbers leading the way. Livongo also continues to rapidly increase operating leverage and improve the bottom line. Just check out these progressions for the last five quarters (oldest to most recent):

OpEx as a % of Revenue: 99.2%, 91.0%, 85.2%, 78.1%, 70.7%

Operating Margin: -28.9%, -21.7%, -10.2%, 1.1%, 3.7%

Net Margin: -27.5%, -21.2%, -7.2%, 4.5%, 5.6%

Adj EBITDA Margin: -26.7%, -19.8%, -8.4%, 3.2%, 5.5%

EPS: -$.49, -$.46, -$.05, $.02, $.03

Livongo is truly firing on all cylinders right now. From a performance standpoint, it’s a double-digit grower at a $300M+ run rate operating ahead of its own estimate for sustained profitability by 2021. From a business standpoint, LVGO is a cutting-edge platform with a very timely solution for today’s healthcare challenges. The COVID-19 experience has forced the world to take a hard look at healthcare delivery, particularly with regard to monitoring patients and keeping them healthy. Livongo is almost perfectly positioned to take advantage of this movement in our connected, data-driven world. The company finds itself “being asked to accelerate launches to deliver services” and believes “remote monitoring is rapidly becoming the new standard in health and care.” Founder and Executive Chairman Glenn Tullman delivered the money quote for just how big this opportunity could be:

”And if you like telehealth, you'll love remote monitoring because telehealth is after there's a problem. Remote monitoring is preventing the problem in the first place, keeping people out of environments that might be dangerous.”

Those are strong words, but Livongo appears to have the goods to back them up. It is often hard to quantify the ROI for preventative programs because hypothetical savings are tougher to measure than actual revenue. Livongo has worked hard to collect data proving its value add up front. LVGO’s platform is quickly proving to provide better outcomes for both patients and insurers. Now wait just a darn minute! Patients and insurers on the same side!? And both happy?!? In the US healthcare system?!?!? That’s a win-win arrangement in which I’m happy to participate. Happy enough in fact that I immediately increased my position another ~3% after what I thought was a stellar quarter. So far, so good. LVGO’s 2020 is quickly shaping up to be a monster year.

OKTA – What can I say? Okta gonna Okta. The company reported its usual reliably solid quarter on 5/28. The top line included Okta’s typical $9-$10M beat, which meant $182.9M in revenue and a slight acceleration sequentially to 46.0% growth YoY. Subscription revenues also accelerated slightly to 48.3%. Subscriptions clocked in at a record 95.0% of total revenue, and the 121% expansion rate was the highest in 7 quarters due to “strong customer upsell”. Billings growth held steady at 42.3% and RPO grew 56.6% to a whopping $1.24B. Customer growth contracted slightly on a percentage basis, but the raw adds were right in line with past quarters despite some COVID-related slowdown in closing deals. All in all, Okta’s top line business appears to be holding up quite well.

The bottom line continues to show steady improvement as well. Profit margins continue their march toward breakeven. Net margin was -4.4% vs -17.1% last year and operating margin was -6.7% vs -19.9%. Cash flows were excellent as the company posted records in both operating cash flow ($38.7M; 21.2% margin) and FCF ($29.8M; 16.3%). Some of that was due to reduced expenses that should tick back up post-virus, but the overall trend reinforces Okta’s strong business model. Management anticipates some sales cycle headwinds the next two quarters but says “decisions have been pushed out to a later date rather than canceled.” It is anticipated things should return to normal by the end of Q4.

Management reaffirmed its “conservative” FY revenue guide (which was my only quibble as I would have preferred a raise) while improving the FY operating loss outlook. The operating loss guide for Q2 is -$4M, meaning a reasonable beat could put Okta on the verge of its first breakeven or even slightly profitable quarter. Considering what is going on the world, the company seems none the worse for wear. In fact, the CEO stated:

“We have no doubt that a much higher percentage of workforces will be connected remotely and we see that as an inevitable long-term trend. Actions that organizations are taking today are accelerating that long-term arc toward using more technology for more flexible work. That's a positive trend for the world and for Okta.”

While I can’t say Okta is my most dynamic holding, it has been an excellent investment and more than earned its current spot as a portfolio stalwart.

ROKU – Roku gave us two updates this month. The first was the company following through on its dataxu acquisition by launching the OneView Ad Platform. This new product lets advertisers plan, buy and measure ad campaigns across Roku and other platforms including OTT, desktop and mobile. In the release Roku estimates OneView’s reach as 4 out of every 5 homes in the U.S.

Roku had previously used a more traditional direct sales model to handle most of its ad inventory. This new platform will allow marketers to directly monitor and optimize their own campaigns. The main features are below:

Better identity solutions – access more accurate TV audience data powered by Roku’s direct consumer relationships

Deeper consumer insights – plan and measure using unique linear TV data from ACR on North America’s #1 licensed TV OS

Proprietary audiences – activate more than 100 unique segments based on data from the No.1 TV streaming platform in the U.S. by hours streamed according to Kantar

Instant OTT forecasting – calculate OTT ad inventory availability in seconds to buy advertising sold by both Roku and other publishers across OTT

In-flight attribution tools – optimize reach, frequency and performance across OTT, linear TV, desktop, and mobile campaigns

Guaranteed outcomes – guarantee demographic delivery or business outcomes such as website visits or mobile app downloads

As Roku continues to gain both mind and market share, OneView should be a valuable tool for optimizing exposure and monetizing its userbase. Anything that increases efficiency and stickiness is fine by me. I like this move.

That announcement was followed by Roku’s 5/7 earnings release. The headline numbers were strong and in line with their April preannouncement. Total revenue of $320.8M represented 55.2% growth, which is a significant acceleration both sequentially (vs 49.1%) and YoY (vs 51.3%). In fact, it was Roku’s largest Q1 revenue growth rate in five years. Platform revenue growth also accelerated sequentially to 73.4% and now accounts for a record 72.5% of total revenue. Streaming hours, active accounts (now >40M) and average revenue per user all continue to increase steadily. Roku did post income and EBITDA losses, but the final numbers came in better than expected even as the company continues to fund platform and international growth.

On the hardware side, player revenue came in ahead of expectations and “…sales of both Roku players and Roku TV models remained very healthy year-to-date, despite some supply chain and retail disruptions.” The company noted that after some early factory closings current production is close to normal capacity. Roku’s operating system continues to power more than 1-in-3 smart TV’s sold in the US and more than 1-in-4 in Canada. The company is also pleased with its early international efforts in Mexico, Canada, Brazil and the UK. As pointed out multiple times, hardware is not a revenue driver for Roku but rather an avenue for increasing platform access and in turn the number of viewers. In that respect, COVID-19 doesn’t appear to have drastically affected Roku’s operational plans for acquiring more eyeballs.

Digging deeper on the platform side, the underlying trends are about as expected. Ad dollars have been pressured while content distribution and user engagement have surged. Management stated the acceleration in accounts and viewership seen in the final month of Q1 has continued into Q2. They also noted some virus-related ad cancellations have been offset by new business coming from the elimination of live sporting and entertainment events on traditional TV. While remaining uncertain about the future, management did remark that March’s initial cancellation surge had stabilized in April. They now expect “our ad business will continue to grow substantially [bolding mine] on a year-over-year basis, albeit at a slower pace and lower gross profit than we originally expected for the year”. Platform gross margin of 56.2% was slightly lower than anticipated due in part to COVID-19’s impact on video ad sales and sponsorships. As with several recent tech trends, ROKU does see a possible virus silver lining where these temporary ad declines are more than offset by “accelerating the shift to streaming by both viewers and the industry”. As CEO Anthony Wood wrote in his closing statement of the Q1 shareholder letter:

“Much uncertainty remains, but a few things are increasingly clear to us: streaming, and the ease and value it provides, is more relevant to consumers than ever; overall advertising expenditure in the U.S. is likely to fall in 2020, but we expect our ad revenues to still grow substantially year-over-year; Roku is well positioned to be an increasingly valuable partner as brands decide how to invest marketing resources most effectively; and, our outstanding talent is keeping our company highly productive. Although the Streaming Decade began differently than anyone could have imagined, we are confident the fundamental shift to streaming will continue, perhaps even faster than previously expected.”

That statement is as thorough an explanation as any as to why I plan on holding shares at least through the next report. We all get caught up in stock price – myself included – and Roku’s has been all over the place in the year-plus I’ve owned it. Roku helped lead the charge for my 2019 returns but has been a notable drag in 2020. The bears seem to focus on the steady losses and the bulls seem to focus on the notable revenue and platform growth at scale. Personally, I am still intrigued enough by how the company sticks to its plan and has executed on just about everything it has initiated. Listening to the call it doesn’t sound to me like they are letting any short-term macro issues affect their long-term vision.

In the big picture I continue to bet on Roku’s persistence eventually paying off as we pass through and then out of COVID-19. I’m banking on the continuing viewership surge translating to better bottom line leverage starting next report. If that doesn’t come to pass, I’ll be seriously revisiting this position. Roku is becoming similar to my 2019 Square and Twilio experiences in that my interpretation of the numbers just does not match what the market is telling me. As this post on a Motley Fool message board so eloquently puts it – and I would have to agree – Roku’s story just doesn’t seem to be holding up the way I think it should. At some point the opportunity cost of waiting this out will be simply too hard to ignore given my other choices. However, I’m choosing to hang in there for now.

TTD – A long-time holding sold in April, the Trade Desk posted a quarter about as expected on 5/7. The company continues to spit out a steady profit, and CEO Jeff Green continues to be one of my favorite execs. He is smart, confident, crazy articulate and knows his market like the back of his hand. To no one’s surprise advertising is experiencing headwinds, as almost every firm in that sector has pointed out this earnings season. TTD has adapted and seems well-positioned to grind through. However, some uncertainty does remain. I made a point of tuning in to this report as a review of last month’s sale decision. After doing so I can’t say I have more conviction in TTD than any of my current holdings, so the decision still makes sense to me. TTD remains an excellent company though and will continue to hold a prominent spot on my watch list in case something changes.

WORK – As we enter June, this is turning into a pretty simple thesis. Slack finished the month strong but hasn’t received quite as much love as most of its peers during this most recent SaaS run. The market seems to be waiting for WORK to prove it can be a profitable, mission-critical work platform rather than just a cool niche product for the tech savvy. The recent remote work movement is just about the perfect environment for testing Slack’s value add for the broader business world. In some ways its 6/4 earnings report is setting up as a binary event. Either the metrics prove WORK deserves a bigger premium or the stock risks being relegated to the sector’s second tier. I’m obviously hoping for the former. The latter outcome would likely initiate a fairly quick watch list showdown.

ZM – Zoom spent just about the entire month following through on its pledge to shore up security issues. First, ZM proved its commitment to this challenge by acquiring Keybase, a secure message and file-sharing service. Given the press release headline specifically notes the “Goal of Developing the Most Broadly Used Enterprise End-to-End Encryption Offering”, it appears Zoom has decided to leave nothing to the imagination as far as the motivation behind the move. Next, it partnered with Secure Code Warrior to help with secure coding for Zoom’s development teams. These efforts have calmed many who had previously backed away from the service, including the NY Attorney General and New York City public schools.

On the development side Zoom announced plans to open two US-based R&D centers in Phoenix and Pittsburgh. Recruiting for software engineers will begin immediately, and new hires will work from home until the offices are built. The plan is to hire up to 500 new engineers between the two cities. The release implies Zoom will work closely with local universities Arizona State and Carnegie Mellon to build out the program. It is important to note few companies are expanding this aggressively in the current COVID environment. That makes it very easy to interpret this commitment as a sign Zoom doesn’t see its recent growth slowing any time soon. That’s perfectly fine by me.

I know Zoom’s PR response to its recent challenges has gotten mixed reviews. However, I can’t help but admire how they’ve risen to the challenge. After Eric Yuan’s heartfelt apology approach fell mostly on deaf and cynical ears, Zoom appears to have pivoted to “OK, well then screw you and watch this!” Since then the company has not only acted assertively but overcommunicated while doing it. While Yuan keeps smiling on the main stage, his cohorts behind the scenes have rolled up their sleeves and really gotten after it. As a shareholder I can only heartily say, “You go, girl!”

As May wraps up, Zoom seems to have very much regained its mojo. In my opinion it’s not a moment too soon because Zoom’s 6/2 earnings report might just be the most fascinating of the season. Hang on tight everybody. Here we go…

My current watch list…

…in alphabetical order is:

BILL – Still more of a curiosity for me. Core revenue growth is impressive, but the overall numbers aren’t as dynamic as some others. Saw a big post earnings jump before drifting back down. I’ll wait until after their mid-June IPO lockup expiration to reassess.

DOCU – Docusign seems to be in the right place at the right time with the contract lifecycle management (CLM) platform it released last year. This CLM offering has seen a usage spike with remote work and is proving to be very efficient in replacing some traditionally clunky manual processes. Given its ease of use, I’d have to think much of this recent uptick has a chance to stick post-COVID.

EVBG – It’s not hyper growth but does have big tailwinds for its crisis management platform. Some European regulatory requirements for mass notification should help its international business through 2021.

FSLY – The most intriguing name here. I had concerns how long it would take to overcome the consistent double-digit loss margins at only 40% growth with mid-50’s gross margins. They crushed it this quarter and guide to 56% top end revenue growth in Q2. Gross margins should likely climb a tick as well. It is a different profitability thesis if Fastly has truly moved to a new growth and/or gross margin tier. However, it’s worth pointing out the 9 enterprise customers signed last quarter to get to 297 total was their lowest add in seven quarters. That’s a far cry from what companies like CRWD or DDOG are doing as far as customer adds. A lot of this quarter’s bump and next quarter’s guide is due to current customers spending a ton more, which should continue short-term. The question is how much of this growth will remain post-COVID.

MDB – I believe in the No-SQL movement, so why haven’t Mongo’s recent numbers backed it up? From a stock price standpoint, Mr. Market doesn’t seem to care. With everything moving online, will MDB’s usage pick up enough to reverse their recent downward growth trend and weak FY guide? Our first hints should come when Mongo reports on 6/4. I’ll be paying close attention to the growth of their Atlas product and Atlas’s revenue contribution as a percentage of Mongo’s total.

NET – Another name jockeying near the top of this list right now. I like what I know about the tech so far. However, its sales process is a little more top-down than some other names. That has generally made deals tougher to close in this environment. Cloudflare posted a solid earnings report even if it didn’t see the recent usage uptick others have with the move online. Its new virtual firewall product has seen strong early adoption (1,000+ customers) under a program that makes it free through 9/1. That’s pretty impressive and could create a coiled spring effect on revenues at the end of 2020 and into next year. NET is definitely one to watch, but I’m wondering if the wait for firewall revenues might make it more of a name for 2021. I’m still thinking about this one and am open to other opinions.

SHOP – Shopify’s a beast even at the insanely high price. If I had a long-term buy and hold portfolio, this would probably be a feature name.

TTD – See my comments up top.

TWLO – I sold it in October due to questions about organic growth and Flex adoption. It drifted down my watch list in the months since. This quarter alleviated a lot of those issues, causing a huge jump in price the last few weeks. It might be time to revisit Twilio, especially if the optionality they’ve created in their offerings is starting to bear fruit.

And there you have it.

May turned out to be another astounding month. While the everyday world openly struggles through the effects of COVID-19, the markets just keep shrugging things off. That seems even more true for the pocket of tech companies on which I tend to focus most of my attention these days. These companies were already benefitting from a secular trend toward an online, digital world. That move has only amplified as remote work and digital interaction has become the immediate norm. It has been a seismic shift that happened very quickly. Microsoft CEO Satya Nadella summed it up best by commenting that MSFT has seen two years’ worth of digital transformation in just two months. Below is the effect in chart form for the area of ecommerce:

While it is true some firms might see only a temporary boost, it is becoming more and more apparent many are seeing the accelerated effects of a transformation that was already occurring. That should obviously benefit those fortunate enough to hold those names.

As far as my portfolio, May ended as my best single-month return ever. I somehow touched a new all-time high (ATH) intraday on 5/11 before blowing that away on 5/12 to close at +29.0% YTD and +99.5% since 1/1/19. That means I went from an ATH on February 19 to an almost 40% drawdown to a new ATH in a span of just 82 days. Can anyone say volatility?!? I experienced a couple more peaks and a short pullback before a +6.6% day on 5/29 leaves me at a new ATH of +39.2% and +115.3% as I type. Remarkable stuff.

On one hand it seems absolutely absurd my portfolio should be performing like this given what is going on in the world. However, when I stop to think maybe it is not so ridiculous after all. As detailed above, many of these companies are at the forefront of a massive global shift occurring right before our eyes. Who am I to fight the tape? Besides, there are plenty of others out there whose 2020 performance has been MUCH better than mine. It’s just a matter of continuing to identify and hold the right names.

Time after time we have seen successful investing boil down to some version of the following:

Select a style that fits your temperament and goals.

Learn a thoughtful process within that style to select quality investments.

Make regular purchases using money you do not need for living expenses.

Find the intestinal fortitude to stick with your plan through the inevitable market swings (both up and down).

Let history and compounding do their thing.

It seems soooooo simple, yet it is amazing how emotionally and psychologically difficult it can be to stay the course. The good thing is the longer I am in the market the more I come to appreciate the timeless reliability of this plan for those who can pull it off. When you better understand what you own and more importantly why you own it, it is infinitely easier to separate real from noise when the inevitable drawdowns occur. I remain ever so grateful to those I continue to converse with and learn from along the way.

Thanks for reading and please continue to do the right things to keep everyone safe and healthy. Also, don’t forget to mix in a bit of empathy, patience and understanding for those around you as we continue to work this out.

I hope everyone has a great June.

Loved reading this, especially the detailed breakdown of the numbers. Thanks!