November 2024 Portfolio Review

Total Return: +35.9% YTD (+9.4% vs S&P)

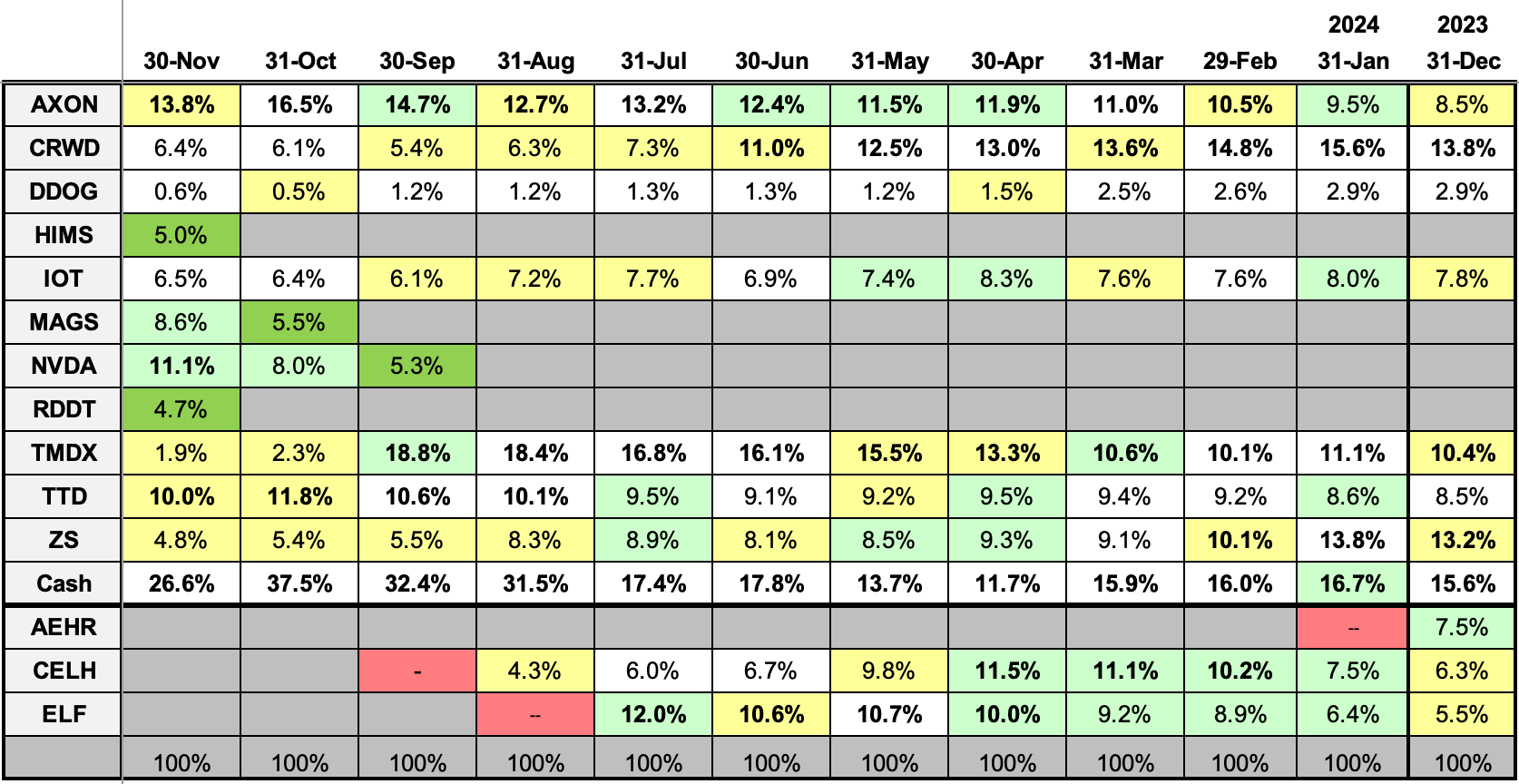

2024 Results:

2024 Monthly Allocations:

Key:

darker green: started during month

lighter green: added during month

yellow: trimmed during month

red: position exits

positions >10% in bold

*Please note: I rolled an old 401K worth ~2.5% into the cash balance of this portfolio to start 2024. I’ve shaded the January cash cell to make sure the new cash is represented accurately (and honestly to remind myself as well).

Past recaps:

December 2018 (the one that got things started)

December 2019 (contains links to all 2019 monthly reports)

December 2020 (contains links to all 2020 monthly reports)

December 2021 (contains links to all 2021 monthly reports)

December 2022 (contains links to all 2022 monthly reports)

December 2023 (contains links to all 2023 monthly reports)

Stock Comments:

Lots of action this month…

AXON 0.00%↑ – Axon posted what I thought was yet another quality report November 7. Sure, you might quibble a bit with this quarter’s cloud growth or new ARR, but the overall thesis looks firmly intact.

Post-earnings, we received even more to get excited about. First, Axon announced a nationwide contract supplying more than 10,000 body cameras to the Royal Canadian Mounted Police. This not only gives Axon another widely recognizable customer win but should provide even further validation with other Canadian national and local agencies.

The company then received FedRAMP approval for its new Draft One and Axon App offerings. For those familiar with cybersecurity, this important US Federal government designation means a company’s products have met rigorous testing and auditing protocols for safe use in cloud environments. This approval automatically expands the use cases in which Axon can be considered by any current or future Federal customers. Nicely done.

Axon enters December as our portfolio’s clear winner heading into 2025.

CRWD 0.00%↑ – CrowdStrike’s November continues a string of very busy months. First, the company expanded its deal with European partner Ignition Technology. An arrangement originally covering the UK and Nordic countries will now extend to Ignition’s customers in Ireland as well.

Next, CRWD announced a new AI Red Team Service. This offering provides customers “with comprehensive security assessments for AI systems, including LLMs and their integrations, to identify vulnerabilities and misconfigurations that could lead to data breaches, unauthorized code execution or application manipulation.”

CrowdStrike then acquired SaaS security company Adaptive Shield. This tuck-in makes CrowdStrike the only company “to provide unified, end-to-end protection against identity-based attacks across the entire modern cloud ecosystem – from on-premises Active Directory to cloud-based identity providers and SaaS applications – delivered from a single, unified platform.”

Lastly – and probably most importantly – CrowdStrike delivered what I thought was a solid Q3 earnings report November 26. While July’s faulty update and resulting global crash was a major misstep, CRWD appears to have not only stabilized its business but even begun regaining its pre-crash momentum in some areas. Given the uncertainty into this report, I’d say the results more than held their own. I exit the quarter very comfortable with our current position.

DDOG 0.00%↑ – I’d call Datadog’s November 7 Q3 report another “good enough” top line with some concern in the underlying trends. While you can’t help but admire DDOG’s operational efficiency, there is only so much bottom line you can squeeze from a moderating customer base and slowing RPO. DDOG is a solid company. The question is whether it is one of the best companies we can own. It’s currently our smallest position at a 0.5% allocation. One of the main reasons I still hold it is our remaining shares are all taxable at a $35.24 cost basis and I’d prefer to bump the capital gains hit to 2025. I’d say this quarter was good enough to keep those shares hanging around. However, I have a decision to make in January.

HIMS 0.00%↑ – A fast-and-furious new position. Hims & hers is a telehealth provider specializing in sexual health, dermatology, mental health, and weight loss. Its secret sauce – or at least the way it is attempting to differentiate itself – is through a dedicated provider network offering personalized patient solutions. To facilitate these solutions, HIMS has built a network of over 1,000 providers thus far with monthly provider retention rates consistently above 95%.

With its weight loss business surging recently due to a shortage of GLP-1 weight loss medicines, HIMS has posted the following performance the last three quarters (oldest to newest):

Revenue Growth: 46% -> 52% -> 77% ($402M) with a 91% Q4 guide

Subscriber Growth: 42.4% -> 43.4% -> 43.5%

Subscriber Growth using Personalized Solutions: 176% -> 164% -> 175%

Revenue per Subscriber: $55 -> $57 - $67

Free Cash Flow Margin: 4.3% -> 15.1% -> 19.8%

Adjusted EBITDA Margin: 11.6% -> 12.5% -> 12.7%

This was HIMS’ first quarter in which more than 50% of total subscribers were using a personalized solution through its platform. In addition, the company has been GAAP profitable the last four quarters and sits on $254M in cash with no debt. There’s lots to like.

This seemed like a great move when the stock surged from $20 to $29 following its November 4 earnings report. Then the roller coaster ride began. HIMS’ recent performance apparently caught the attention of Amazon, which announced it will be redoubling its efforts to provide telehealth and pharmacy services to its enormous Amazon Prime customer base. In fairness, Amazon has been offering some version of telehealth for a while now. The question is how well HIMS’ personalized experience will let it defend its turf. The stock immediately tanked all the way back below $20 on the news. After noticing weight loss isn’t among the new services AMZN is offering, I decided I liked the quarter enough to stick around and see if the market overreacted.

Since then, the stock has soared back above $30 to new all-time highs. It appears the market:

realized AMZN is not competing with HIMS’s weight loss product just yet; and

liked the fact Donald Trump nominated Marty Makary to head the US Food and Drug Administration. Makary is currently…wait for it…Chief Medical Officer of Sesame, a telehealth platform offering GLP-1 weight loss compounds. That should bode well for HIMS being allowed to continue selling its GLP-1 alternatives.

Yeah, this one looks like it’s going to be a bit volatile. In the end though, I find the numbers too difficult to ignore. I’ll be keeping this position sized accordingly as we get more insight into where things are headed.

IOT 0.00%↑ – Samsara’s November featured the unveiling of several new features at the company’s first Go Beyond London customer conference. The additions include:

Connected Training providing data-driven training and feedback for drivers

Low Bridge Strike Alerting using sensors to double check vehicle heights against upcoming bridges

Electronic Brake Performance Monitoring

Privacy Mode allowing Samsara’s video-based safety solution to keep safety sensors active even if the video cameras are not engaged

As usual, these new offerings are a direct result of company data and customer feedback. Given IOT’s laser focus on providing measurable ROI for its customers, I’d expect positive contributions from all of them going forward.

We’ll learn more when IOT reports December 5.

MAGS 0.00%↑ – No real comments on this one other than I’m happy to own it. MAGS is an ETF tracking the Magnificent 7 stocks (NVDA, GOOGL, MSFT, AAPL, AMZN, META, and TSLA). I trimmed a bit early this month when it ran about 10% in a week (mostly due to TSLA), but ended up being a net buyer as things faded in the second half of the month. I’d prefer less cash heading into 2025 and see this as a place to put some to work while waiting for more attractive opportunities.

NVDA 0.00%↑ – November 20 was our first earnings report owning Nvidia. Top to bottom I thought it an all-systems-go report. NVDA continues to be the dominant picks and shovels play in the current global AI race. When Mr. Market’s main complaint is you’re not making one of the world’s most demanded products fast enough, I’d say you’re in a pretty good spot. I exit the quarter happy to keep NVDA as one of our larger positions.

RDDT 0.00%↑ – A position started shortly after the company’s stellar October 29 report, Reddit is a moderated online message board platform which makes its money through targeted advertising to its posting audience. I’ve started this position for two reasons.

The first is the numbers (oldest to newest):

Revenue Growth: 48.4% -> 53.6% -> 67.9% with a 60.1% Q4 guide which should be beaten

Non-GAAP Op Ex as a % of Revenue: 84.6% -> 75.5% -> 63.1%

Adj EBITDA Margin: 4.1% -> 14.0% - > 27.0%

In addition, Reddit has churned out significant free cash the last three quarters while just delivering its first-ever profit with $6.8M in GAAP Operating Income, $29.9M in GAAP Net Income, and $94.1M in EBITDA. Not too shabby.

The second factor leading me into RDDT is positive commentary from The Trade Desk CEO Jeff Green on tailwinds in the advertising space. I’ve owned The Trade Desk for most of the last six years and have come to trust Green’s instincts. With that backdrop, I decided to augment our TTD position with a smaller adtech firm growing at a much faster rate (I considered faster growing Applovin as well but am just not sure how much room APP has to run at a market cap north of $100B).

What can I say? I’m a sucker for fast growing companies hitting the inflection point where leverage finally scales enough to start throwing off cash flows and profits. Reddit appears to be right in that sweet spot, so I’ve decided to grab a starter position.

TMDX 0.00%↑ – I saw no news on TransMedics this month, but did trim our position slightly by selling shares in a secondary account to help start RDDT. I’m content to sit on the rest for now.

TTD 0.00%↑ – I was hoping The Trade Desk’s November 7 report would be the first step in a big second half performance. Instead, it ended up being another boringly solid showing with the results and guide both roughly in line with my expectations.

Post-earnings, The Trade Desk announced the release of Ventura, a new streaming TV operating system. TTD will partner directly with smart TV manufacturers and other TV aggregators to deploy Ventura in their devices. The system will let TV manufacturers ease “frustrating user experiences, inefficient advertising supply chains, and content conflicts-of-interest.” This in turn will create cleaner inventories for advertisers and more relevant ads for viewers. The press release makes it clear TTD has no intention of owning any TV content, like say Roku (which would be a concern in my opinion). Ventura is simply a vehicle for a more holistic streaming experience for both advertisers and viewers. In that respect, Ventura fits right in with TTD’s track record of creating better, more efficient digital advertising environments.

All in all, The Trade Desk continues to expand partnerships and gain market share through it best-in-class platform. If I had to speculate on the market’s blah reaction post-earnings, I’d say the comments on muted political spend in a polarizing election led to some profit taking after the stock’s run to all-time highs into the report. No matter though. In my opinion, the quarter was business as usual.

For now, I’m viewing RDDT and TTD as an advertising pair in our portfolio with a combined allocation target of 15-20%. Going forward I’ll probably look for opportunities to lower TTD a notch while raising RDDT to shift some funds into the faster grower.

ZS 0.00%↑ – Zscaler the company recently announced improvements making it easier for customers to extend its Zero Trust protection to data distributed in different locations, data centers, and/or public clouds. ZS the stock had a nice month as the market recently rotated some money into cybersecurity names.

We’ll hear more when ZS reports December 2.

My current watch list…

…is monday.com (MNDY) and MercadoLibre (MELI) with a softer eye on Applovin (APP) and Shift4 Payments (FOUR).

And there you have it.

Gotta love a bunch of strong earnings reports in an enthusiastic market. As 2024 reaches its final stages, I’m comfortable with how 2025 is shaping up. I’ll ideally carry less cash next year, and that’s a big pre-New Year’s resolution. However, it’s hard to complain too loudly when that idle cash has been earning close to a 5% return most of the year. With interest rates now starting to turn however, I look forward to putting that cash back in play.

As usual, thanks for reading, and I hope everyone’s holiday season is off to a joyous start.