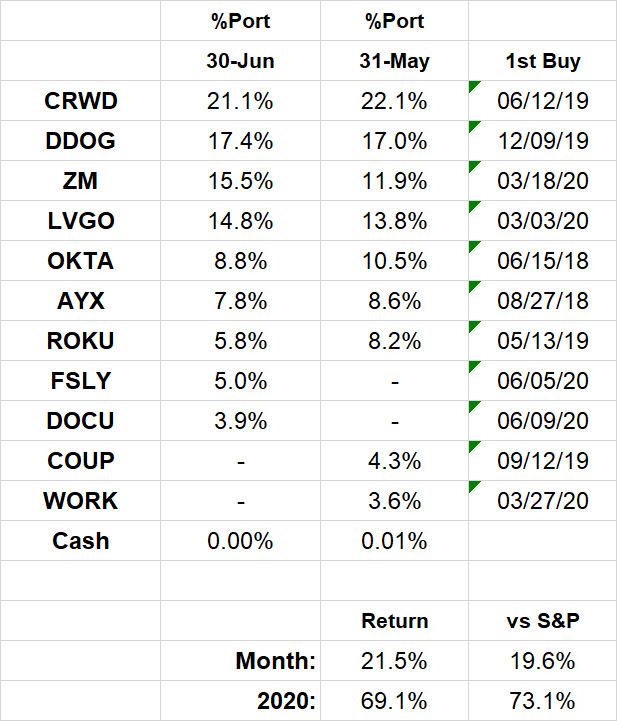

June 2020 Portfolio Review

Total Return: +69.1% YTD (+73.1% vs S&P)

This is not normal.

I mean, it’s perfectly normal for stocks to go up and down. It is also normal for the market to rise more than it falls over time. However, the extreme moves of the last few months have been anything but ordinary. In fact, the last few months have given volatility a whole new meaning. Algorithmic trading, 24/7 social media and a newfound legion of fledgling investors are determining this market’s winners and losers at breakneck speed. Those companies which have adjusted to COVID-19 are being rewarded. Those which haven’t are being punished. And those few helping lead the world’s current transformation are seeing their values absolutely skyrocket.

Where does it end? I have no idea. The market will undoubtedly find a new equilibrium at some point. It always does. For now though, I’m perfectly content to sit back and enjoy the ride.

2020 Results:

June Portfolio and Results:

2020 Monthly Allocations:

Key:

darker green - started during month

lighter green - added during month

yellow - trimmed during month

blue - bought and sold during month

red - position exits

Past recaps:

December 2019 (contains external links to all 2019 monthly reports)

Stock Comments:

June is my third consecutive month ending with nine stocks. However, I did make some changes. As my portfolio evolves, my last couple slots have morphed into ~3-4% starter positions in companies I feel have the potential to earn bigger allocations. Livongo and Datadog have had very successful runs from these spots. Other names have not worked out quite so well. Coupa and Slack held these positions the last three months. Unfortunately – SPOILER ALERT! – both lost their status when two watch list names exited earnings with what I believe are better prospects. Those spots now belong to DocuSign and Fastly.

One of the side effects of this dynamic is a continual showdown between my bottom holdings and the top of my watch list. That in turn has led to a decent amount of back end churn. While I am still honing this process, it has basically turned into an earnings-to-earnings call. For better or worse, this quarter’s results have me believing FSLY and DOCU have more upside than WORK and COUP. I originally staked slightly over 7% of my portfolio on that bet, and it has quickly appreciated to ~8.9%. Last quarter this process led to swapping some COUP for LVGO along with dropping SMAR for adds to AYX and DDOG. Those moves have worked out. In fact, it has really worked out with LVGO since the conviction I’ve gained has led to a much larger position and considerable paper profit so far. On the other hand, my partial sale of TTD to purchase WORK is clearly not my finest hour.

To ensure this madness has some method, I am logging these decisions. In a vacuum they have been profitable so far, although it is much too early to draw any firm conclusions. The larger benefit seems to be a reasonable way to sample new names that have later become core holdings. I can't ignore that as a positive advantage.

It does have me thinking though. Is this too undisciplined? Is there too much rationalization and not enough patience? I guess the money question is just how long should one hold a lower conviction stock when watch list names come knocking at the door? While I can clearly explain my reasoning, I also know we are strongly biased toward justifying our own actions. I’m not immune. When it comes to my core holdings, I believe I have a thorough process that is appropriately ruthless when needed. I would say the same for my watch list. My present wonder is whether I have the right mix of ruthlessness and patience where the two blend together. I don't feel strong regret for my misses and consider myself lucky to be wired that way. This is more about seeing if I can learn something from my past to create a better process for the future. So how do others manage this trick? I’m all ears.

AYX – Alteryx had a solid month (+14.1%) on limited news. The only notable announcement was a release detailing two new offerings – Alteryx Analytics Hub and Alteryx Intelligence Suite – augmenting its broader product line. The recent price action suggests the market has digested last quarter’s headwinds warning without much penalty to the stock. This makes sense since AYX’s long term thesis remains very much intact. Move along, folks. There’s not much to see here…

COUP – This was a bit of a tough call. As I wrote in May, “The efficiency of Coupa’s platform has almost certainly been invaluable to its users these last few months. The question is just how much new business COUP will land given the likelihood many potential customers are currently tightening their belts.” After Coupa’s 6/8 report, it appears the belt tightening will affect the next couple quarters at least.

This quarter itself was a strong one. Revenue grew 47% to a record $119.2M. Subscriptions grew 45% and continue to account for ~89% of total revenue. As usual, Coupa showed strong operational leverage by posting positive operating (12.5%) and net (12.1%) margins for the eighth quarter in a row. It also posted its third consecutive quarter of at least $20M in free cash flow. COUP continues to be a lean, profitable company.

Unfortunately, the fallout from COVID-19 is going to affect the remainder of 2020. Management noted "spend sentiment across most industry verticals has fallen sharply." In addition, they say “many of our customers and prospects are now operating with significant headwinds, especially those in industries highly affected by the pandemic, making it difficult to predict the timing of when deals will close.” Given the uncertainty, “our current operating thesis is that the macroeconomic environment will remain challenging for at least Q2 and Q3 with things beginning to open up more broadly in Q4.”

Coupa also has tougher comps coming in Q2 since last year included both an acquisition and a large one-time pull forward from business with the USPS. While management has left all kinds of wiggle room to beat and raise in 2020, they significantly reset next quarter’s bar to make it happen. Even a reasonably normal beat would drop growth from 47% to 32-33%. Along those same lines, FY20 revenues that grew 49.7% will now have to hustle to cross management’s own 30%+ goal for FY21. I’m fairly confident they will make it, but that’s still a bit more slowdown than I was expecting.

In the big picture I think Coupa is a very good company. Its platform is proving crucial for existing customers, and the company will likely exit the pandemic in a strong business position. However, having such a condensed portfolio means I don’t have to carry a company projecting headwinds when others don’t have those challenges. I know the current market is giving a pass to many companies whose sole blemish is short-term COVID headwinds. However, I decided AYX and OKTA were better representatives of this subset than COUP. Consequently, I turned my Coupa gains into new shares of DOCU.

CRWD – With CrowdStrike being my #1 holding, I was paying extra close attention to 6/2 earnings. Once again, CRWD did not disappoint. It posted strong top and bottom line beats while expressing considerable enthusiasm for the future. Revenue growth remained strong at 85.3%, subscriptions grew 88.7% and annual recurring revenue increased 88.2%. Overall gross margins jumped to 75% from 70% last year and subscription GM increased to 78% from 73%. Those are outstanding figures for any company, but especially one with a run rate now north of $700M. CRWD’s top line looks like a hyper growth machine from almost all angles.

But wait, there’s more!

Not to be outdone, CrowdStrike’s bottom line is also getting sexier by the quarter. The highlight was the first positive operating income in company history at $1.2M and 1% margin versus -$12.9M and -23% last year. Expenses as a percentage of revenue dropped to 75% from 93% last year despite “investing aggressively in our business during the quarter.” Finally, cash flows soared. Operating cash totaled $99M and free cash flow came in at $87M for an eye-popping 48.9% FCF margin. What’s not to like about that?

Security is becoming mission critical for virtually every business, and CrowdStrike is seeing huge benefits as a result. Companies were already transferring many security systems from on-premise to the cloud. This trend has only accelerated with the huge surge in remote working. Total customers increased 105% YoY to 6,261, which extends CRWD’s streak of triple-digit customer growth for every quarter on record. The percentage of those customers using at least 4 modules hit 55% and the number at 5+ was 35%. More important in the present climate, CrowdStrike “closed the vast majority of this quarter’s 7-figure deals in the second half of the quarter after the shelter-in-place orders were in effect, which is consistent with prior quarters”. The CEO noted a strong increase in new business meetings this quarter and a record pipeline at the end of Q1. Finally, the CFO states CRWD has “been able to derive an average of about $3.73 of subscription ARR for every $1 spent on an initial incident response or proactive service engagement as of January 31, 2020.” So, customers are not only paying for CRWD’s initial help but gladly ponying up for continued subscriptions after the fact. That is about as sticky as you can get in my opinion.

In the continual search for companies positioned for success both during and after COVID, CrowdStrike seems to very much fit the bill. Management gave a “de-risked” (their term) guide for 76% top end growth in Q2 along with breakeven operating income. Given its history, I would estimate 80%+ again with another small profit. With record sales and over $1B in cash, CRWD looks perfectly situated to continue its phenomenal success. CrowdStrike remains #1 with a bullet in my portfolio, and I can’t see that changing anytime soon.

DDOG – There were two positive pieces of Datadog news this month. The first was DDOG achieving FedRAMP status for “low-impact SaaS”. This opens US government clients to Datadog’s products and took effect May 14. My prior FedRAMP experience suggests this is good timing since most government budget and operations planning is done during Q3. I’m curious to see what Datadog can do in this newly expanded government vertical.

The other news was an integration announcement for the new “Amazon Elastic File System…for AWS Lambda on Amazon Web Services (AWS)”. This integration “allows developers to have visibility across the serverless components that power their business and troubleshoot potential issues quickly.” Being a non-techie, I must admit to not fully knowing what that means. However, I do know:

Datadog continues to innovate and expand its presence;

a lot of developers use AWS as their service of choice;

OMG! Amazon likes us!

the market bumped the stock upward when the announcement was made.

So yeah, count me in on both these announcements probably being good things. Go, Dog. Go!

(I Can Read It All by Myself ...")

DOCU – DocuSign is a former watch list stock making its first appearance in my portfolio. DOCU is one of those companies seemingly in the right place at the right time with the recent shift to remote work. A long-recognized leader in eSignatures, DocuSign now has plans on dominating the entire end-to-end process for digital agreements. To that end, in early 2019 DOCU unveiled its Cloud Agreement platform specifically designed for contract lifecycle management (CLM). This quarter’s results suggest DOCU’s efforts to expand its reach are starting to see considerable traction.

Revenue came in at $297M and 39% growth, which is a slight acceleration from +38% last quarter and +37% last year. Subscriptions (+39%) followed a similar path (vs +38% and +36%) and now account for 95% of total revenue. As with most companies hitting its stride, that top line growth is creating leverage at scale. Expenses came in at a record-low 70.8% of revenues with positive operating (7.8%), net (8.1%) and FCF (11.0%) margins. At first glance, DOCU looks like a steady grower moving firmly into profitability.

However, that’s not what has me most interested. What intrigues me more are signs DocuSign may see accelerated business over the next few quarters. Check this out:

Billings growth the last three quarters: 36%, 40%, 59%. They guide for a pullback next quarter, but simply meeting the FY guide would put billings at its highest rate in at least three years. It is clear this metric is in a very good spot.

Growth in customer contract liabilities: 34%, 33%, 43%.

Docusign added 68,000 total customers this quarter after averaging roughly 27,000 the last six. That’s 2.5X.

Docusign added 10,000 enterprise customers this quarter after averaging roughly 6,000 the last six. That’s 1.7X.

Growth in customers with an ACV >$300K: 41%, 41%, 46%.

International revenues grew faster than domestic, coming in at 46% growth YoY to $55M total. DocuSign’s self-service option is available in roughly 150 countries. This could bode well for global expansion.

Net Retention Rate: 112%, 113%, 117%, 117%, 119%.

Reviewing DOCU’s history, this was not just a seasonal spike. It looks instead like a legitimate buildup of customers, contracts and NRR expansion that should positively influence future quarters. DocuSign is strongly positioned to displace several clumsy, antiquated manual processes. As with many other areas, COVID-19 could accelerate that transition. A decent Q2 beat could push growth back to 40%+, and there is a reasonable argument it could stay there for a while if Agreement Cloud adoption and DOCU’s international business continue to grow. DocuSign already owns the bulk of the eSignature market. Management suggests a successful foray into the CLM market could double its TAM to $50B. The CEO stated on its call, “we believe this surge in eSignature adoption bodes well for future Agreement Cloud expansion.” So do I. Therefore, I have opened a small position. So far, so good (+18.7%).

FSLY – As mentioned above, Fastly joined my portfolio early this month after grabbing my other back-end tryout spot. For the tech breakdown, I’d strongly recommend this post and this post at the Software Stack Investing (SSI) blog by Peter Offringa. Offringa has 20+ years of software engineering experience and clearly knows his stuff. All I know is he is excellent at explaining the nuts and bolts to non-techies like myself. If nothing else, that makes figuring out what these companies do much easier. My info thus far seems to suggest Fastly’s tech is in a great spot.

[Interlude: That tech is apparently in an even better spot now. I’m pretty sure 100 terrabits per second is a lot. This layman's article at the Nasdaq site says it basically doubles Fastly’s capacity. If I were you though, I’d wait for Peter to chime in just to be sure. 😏]

On the business side Fastly has an impressive client list along with usage that has spiked in recent weeks. As written previously, I had some concern how long it would take FSLY to overcome its consistent double-digit loss margins at only 40% growth and mid-50’s gross margins. The company responded by posting a strong Q1 with a 56% top end Q2 revenue guide. Given their history and still small run rate, a move to 60%+ is not out of the question. In addition, management stated at a recent analyst event that gross margins will scale as usage increases. It is obviously a much different profitability thesis if Fastly can move to a new growth and/or gross margin tier. If that happens, both the price and multiple could quickly expand even further.

Like most firms experiencing a COVID-19 usage bump, the risk lies in the amount of business that holds post-virus. It is worth pointing out last quarter’s nine new enterprise customers for just 297 total was the lowest add in seven quarters. A rate that low is a valid concern for a company this young. It is also a far cry from what names like CRWD or DDOG are seeing in customer totals and growth. There is also a danger the increased revenue is only a temporary surge in current customer spend, though FSLY’s 133% expansion rate suggests at least some of that trend should continue. Additionally, Fastly’s new Compute@Edge product is heading steadily through beta toward general release, which could provide additional revenues into 2021. My hope is Fastly can add enough clients, retain enough of the surge and implement Compute@Edge quickly enough to offset any usage dip as the pandemic fades. In the end I saw enough positives to take a starter spot and see where it goes. Since that spot is now up 87.1% in less than a month, I’ll readily admit to liking what I see so far.

LVGO – Livongo gave us a couple pieces of news this month. First, the company took advantage of its recent business momentum to grab $475M through a convertible note offering in early June. It originally proposed $400M but interest was strong enough to upsize the amount. I am always in favor of my companies aggressively and smartly continuing to grow. Grabbing extra-cheap money when it is available is the perfect way to do it. No issues there.

The second was a company release detailing two studies Livongo presented at a recent American Diabetes Association event. Not surprisingly, the studies show LVGO’s remote monitoring program can lead to improved outcomes for participants. In and of itself, there is nothing earth shattering in the new info. However, it is yet another example of Livongo quantifying its value add for existing and potential customers. That can only bode well for the future. Being honest, it is hard to find much of a chink in LVGO’s armor right now.

OKTA – This month’s big Okta news was the announcement of a private offering for $1B in convertible notes. Okta will use the funds to pay some capped call transactions while reserving the rest for general corporate purposes. As stated above with Livongo, I rarely take issue with one of my companies raising cheap money. What’s notable here is $1B is certainly a significant haul. I am very curious to see what Okta might have in the offing.

Secondarily, Okta announced a partnership with CrowdStrike, Netskope and Proofpoint to “help organizations implement an integrated, zero trust security strategy”. This appears to be more of a generic collaboration announcement than anything significant, but it is always good to see potential best-of-breed companies sharing ideas. I felt it noteworthy enough to at least mention.

As far as the stock, my allocation has shrunk from 10.5% to 8.8% since 5/31. That is not a loss of faith or even selling a share. It is simply everything else soaring while Okta posted a +2.4% June. When +2.4% is your laggard, you know it’s been a pretty good month. I’ll continue to let these shares ride.

ROKU – Anyone reading my recaps the last few months knows Roku has become a personal battleground stock. That internal battle heated up again after I read this excellent write up on Roku’s Q1 results. While I was fully aware of everything mentioned, this post tied it together in a way I had not considered before. In my opinion, this is one of the best parts of sharing ideas. Different perspectives can really clarify your own thinking. While I’d always understood the bear case, this breakdown left Roku even more vulnerable than I’d originally thought.

After thinking it through, I began chipping away at this allocation by shaving 2% to add to ZM after Zoom’s – *foreshadowing* – somewhat interesting earnings report. I also converted a small portion of my shares into an equal dollar amount of long-dated calls since I feel Roku has one of its periodic surges coming at some point. Subsequent rises in ZM and ROKU have made both moves worthwhile so far. It is important to point out I do not use options very often AND YOU SHOULDN’T EITHER IF YOU DON’T KNOW WHAT YOU ARE DOING. I chose that route here because I still have enough faith in the company to keep a decent amount of skin in the game. However, Roku’s leash is shortening as it continues to lag YTD. Next quarter’s earnings will have major sway on this position.

WORK – Oh well. I wrote last month I saw Slack’s earnings becoming a binary event. The stock would either grab the same premium as other names with recent tailwinds or likely end up relegated to grinding it out in SaaS’s second tier. Long story short, I believe WORK posted a mild disappointment despite what seemed to be an almost perfect environment for proving its worth to the broader business world. The headline numbers were within expectations, and I was initially excited by the Q2 guide. However, after digging deeper I thought the secondary metrics lagged and the call was lackluster. Even though management noted the “all at once shift to work from home concentrated multiple quarters of Slack adoption into a few weeks”, that uptick sure didn’t seem to stand out in the quarter’s results, the FY guide or the rest of management’s comments.

Paid and $100K+ customer growth were both OK but not nearly as impressive as many others in the thick of today’s digital transformation. Slack continues to battle the fact “it’s always taken some time for Slack usage to kind of grow up inside of an organization, for people to get the hang of it, to invite their peers and colleagues for it to spread.” That doesn’t sound like frictionless, viral adoption to me. The kicker was when the CFO stated, “The transition to work-from-home was obviously a major tailwind this quarter and we expect net new customer additions to moderate through the remainder of the year to quarterly levels closer to those observed in fiscal 2020.” He also noted uncertainty in the sales cycle and “less visibility into how IT spending will trend the remainder of the year.” So, in the end this was just a one-shot deal?!? That doesn’t strike me as a disruptive communication platform. Rather, it sounds like a product still fighting to prove it is mission critical rather than useful tool. That puts it closer to the SMAR’s and PLAN’s of the world than CRWD or DDOG. Frankly, that is not what I was looking for.

Despite what I viewed as a wide-open shot on goal, I feel Slack clanged one off the crossbar. Heading into earnings, I viewed WORK as a good risk/reward scenario. Coming out I feel Slack’s thesis is still a bit more hope than execution. When I get that vibe, experience suggests it is time to move on rather than attempt to rationalize my misjudgment. Therefore, I booked the small gains from my March purchase and put the funds toward a new position in Fastly and a tiny add to LVGO. That’s been an outstanding move so far. In total fairness, this switch was just as much FSLY pounding on my portfolio door as any dislike for what WORK might become. WORK goes back to my watch list instead.

[Epilogue: WORK formally launched its Slack Connect program shortly after earnings. YAY! The ability to link external organizations could greatly expand Slack’s use cases and by extension its addressable market. On the other hand, we saw Salesforce say it was going to veer away from its Slack integration and produce its own solution. BOO! A customer deciding to move to its own solution is never good, at least in the short term (think TWLO and Uber). Slack clearly seems to be onto something. However, as management stated adoption continues to be a grind. Let’s see what kind of traction Connect can get the next couple of quarters.]

ZM – That. Was. AWESOME!

First of all, before reading any of my rambling I can’t recommend this excellent recap strongly enough. It is far more thorough than anything I could write and is a MUST-READ for anyone owning or considering Zoom. As for my lesser take…

Even with the rampant speculation thrown around by the market prior to 6/2 earnings, Zoom’s final numbers were absolutely jaw dropping. Just how popular has Zooming become the last few months? Well, the company’s “meeting minutes run rate” jumped from 100 billion at the end of January to over 2 trillion in April. To handle that type of increase on a global scale with nary a hitch is nothing short of astonishing. And when you can pull something like that off, well let’s just say the money pours in.

Zoom demolished consensus estimates with $328.2M in revenue for 169% growth (not a typo). Gross profit increased 131% (again, not a typo). RPO came in at $1.07B, which means a jump of 183% YoY (will you please stop wondering if these are typos?). ZM churned out $54.6M in operating income (17% margin), $58.3M in net income (18%) and a whopping $251.7M in free cash flow. Would you believe that is a 77% FCF margin? How does that even happen?!? I don’t know, but I’ll gladly take it.

Making it even more interesting is that Zoom’s remarkable results were truly a global affair. While business in the Americas grew 150% YoY, international grew a whopping 246% and now accounts for ~25% of total revenue. According to the CFO, “Our global brand awareness has spread more quickly, and we have expanded into more countries than we had originally planned for FY ’21.” I guess that’s what happens when you become a global phenomenon virtually overnight.

The beauty for shareholders is in some respects it looks like this party might just be getting started. Zoom ended Q1 with 265,400 customers with 10+ employees. That figure is up 354% YoY (the most ridiculous non-typo of the bunch in my opinion). It also reported 769 customers with >$100K in trailing twelve-month (TTM) revenue, up 90% YoY. However, some additional context might be needed to keep from selling even that impressive number short. As shown on slide 9 of Zoom’s earnings presentation, the company noted a one-time figure of 500+ new customers onboarded at a rate >$100K in ARR in Q1 alone:

It also listed in the footnotes that number was rounded down to the nearest hundred. While that is at least a 78% sequential increase from 4Q20’s 641 customers, it’s important to note the new adds technically can’t be counted yet since the figure is based on TTM. That means we should expect a considerable surge in the reported number of larger customers in future quarters. Again, jaw dropping.

To make sure all angles are considered, there were a couple minor items from Zoom’s prodigious quarter worth at least monitoring. First, income from customers with fewer than 10 employees grew to 30% of total revenue in Q1 vs 20% in Q4. Since its normal focus is enterprise customers Zoom does expect a shift in its billings mix along with some increased churn going forward. It is also possible at least some new customers will drop the service after the pandemic ends. My guess is Zoom will find a way to live with it since those losses would be smaller customers coming off a MUCH larger revenue base. In addition, gross margins shrunk to 69.4% vs 84.2% last quarter and 80.9% in 1Q20. I guess that is the price you pay when you gift free minutes to over 100,000 K-12 schools in 25 countries during a global pandemic. In my opinion that is a very small nit to pick when weighed against the enormous exposure and goodwill Zoom earned in return. Management expects gross margins to return to at least the mid-70’s fairly quickly in the quarters ahead.

So, what does this mean for the future? Well, CEO Eric Yuan stated on the call, “I think one thing we know for sure is the TAM is bigger than we saw it before.” Ya think?!? Zoom is not only video communications now. It is online education, telemedicine and telehealth. It is also Zoom Phones and Zoom Rooms, both of which should provide additional revenues if a hybrid home/office workplace becomes the norm for many of those 265,400 and growing customers. In a related piece of news, Zoom Phone has now been added to the previous FedRAMP approval for Zoom’s government offering. For a more detailed peek into all the areas Zoom could go, I’d suggest taking a look at this write up. As it clearly lays out, Zoom’s opportunity for continued innovation and an expanded TAM is enormous. Says Yuan of that possibility, “I truly believe video is a new voice. Video is going to change everything about the communication.” I can’t personally say I’m convinced video will change everything, but I do believe Zoom has a chance to come pretty darn close.

No matter how you slice it, Zoom posted a truly historic quarter. Even better, I don’t see many signs of slowing down. As noted last month, the company will build two new US R&D centers that should house up to 500 new software engineers to support the company’s incredible growth. Zoom’s apparently gonna need ‘em since it guides for 260% growth next quarter and 189% for the full year. How many years of business has Zoom pulled forward into the last few weeks? I have no idea. I only know I am glad I own the shares. Upon seeing the earnings release, I immediately sold some ROKU to grab ~2% more after hours. ZM’s allocation steadily continues to grow.

My current watch list…

…in alphabetical order is:

BILL – Bill.com remains more of a curiosity. Core revenue growth has accelerated the last few quarters, but next quarter’s guide suggests a firm slowdown. I’m also not sure how to value the float portion of revenues since lower interest rates likely make that decline as well. I have other names I understand better right now. BILL could fall off this list if next quarter’s earnings don’t excite.

COUP – See above. I can easily see myself back in Coupa at some point.

EVBG – Everbridge is not hyper growth but does have big tailwinds for its crisis management platform. Some European regulatory requirements for mass notification systems should help its international business through 2021. There is some COVID-19 momentum here as well that doesn’t appear to be going away any time soon.

MDB – I thought Mongo’s 6/4 report was more of the same. The recent declines in growth stabilized some, but management suggests headwinds for the remainder of 2020. Despite noting similar customer adoption and churn, revenues are being pressured by lower usage in the present work environment. Overall, I view MDB’s medium-term outlook as more adequate than good. I still believe in the No-SQL movement, but I can’t see Mongo forcing me out of one of my current names right now. It will stay on the watch list at least until usage starts to pick up again.

NET – Cloudflare is probably at the top of this present list. I like what I know about the tech even if its sales process is a little more top-down than I’d like. Its May earnings report was solid even if we didn’t see as much of a usage uptick as some others in the recent move online. NET’s new virtual firewall product is already being used by 1,000+ customers under a program making it free through 9/1. That is impressive and could create a coiled spring effect on revenues at the end of 2020 and into next year. There is a lot to like here.

SHOP – I have the same beast-mode take on Shopify as last month. If I had a portfolio with more holdings, this would likely be a feature name. As it is, I just don’t see as much upside as other candidates on this list right now.

TTD – Ditto for The Trade Desk, which just seems to power onward. CEO Jeff Green has them lined up very well for the inevitable move to programmatic advertising. That being said, I will likely watch for a quarter or two until we have a firmer grasp on the future advertising landscape.

TWLO – Twilio is becoming more intriguing to me. I sold last October due to questions about organic growth and Flex adoption. This past quarter seemed to alleviate a lot of those issues, leading to a huge jump in price. TWLO’s business does indeed appear to be regaining momentum. However, I am holding off at least until the Q2 release since it will be the first comps including last year’s SendGrid acquisition for the full quarter.

WORK – See above. COUP probably has an easier path back into my portfolio at this point.

And there you have it.

Another surprisingly good month. As mentioned in my very first line, this is not normal. In fact, I can’t believe how strange it felt to even type that word. The truth is this might end up being the most abnormal period many of us ever experience, and I don’t just mean as investors. There are some seismic shifts happening in the world right now, far too many to comment on with any type of impact in something as inconsequential as a portfolio review. Nevertheless, I’d be remiss if I didn’t take a moment to request that no matter your age, gender, ethnicity, race, religion, politics or socioeconomic status please do the best you can to make the world a better place. You don’t even need to embrace a specific cause. Do it simply because it is the decent and human thing to do. Please and thank you.

Thanks for reading, and I hope everyone has a great July.

I really appreciate how you present your portfolio, color-coded for exits, entrances, buys and trims. I am still tinkering with my spreadsheet (actually, several sheets of data) and I will experiment with this, too!

First allow me to say that I've been reading your TMF posts because they represent quality interpretaion and organization. Good luck to you,

You raise a question that continues to puzzle me . "How does one manage the trick?" Perhaps no one really succeeds at managing the trick, but some seem to do OK nevertheless. To assist in the process , if indeed it is assistance, I wish to make a few observations, recognizing that I am more of a novice than you.

I think AYX managed to avoid the heaviest headwinds and will plow ahead successfully, I trimmed some as did others but it probably was not necessary. And now the question is when and how much to buy back. Having distributed the funds it is almost moot.

COUP has more headwinds I think. The reentry problem is also tougher.

DOCU Numbers look super. I probably need to have bought more heavily. There is still time but resources are committed.

FSLY You may have noted that beta users for "compute @edge" are very happy with the product. Many of them and others are preparing use cases for 2021. It portends well.

ROKU has bee a disappointment as you noted IMHO it doesn't measure up to the others. I sold out.

SHOP and TWLO- I sympathise. I sold them both. Still don't know if that was an error.

TTD IMHO it looks like a long term winner in the ad market. Big TAM. It may move tortoise like but move it will. IMO if I sell I will regret it. NVDA is also a holding. Similar story

NET This is an enigma for me. Early on I was convinced it was a competitor of and superior to FSLY so I traded FSLY for NET. Then Poffringers articles appeared and FSLY had its great quarter with a very upbeat remarks by the CEO. I realized I had been mistaken and so I switched back and added some. Good run up since then and one can't look back. so I suggest we look forward.

Cheers