August 2020 Portfolio Review

Total Return: +121.0% YTD (+112.6% vs S&P)

au·gust /aw-guhst/ (adjective):

marked by majestic dignity or grandeur

“Majestic” feels a tad strong, but for a super choppy month August turned out to be pretty good. The market and my portfolio had been on a scorching-hot run since late March. The question was whether this month’s earnings would keep the momentum going. Mr. Market showed initial disappointment in many of my names before enthusiastically coming back around as August progressed. My main takeaway is while SaaS generally held up, no company is completely immune to 2020’s weirdness. Logically, I doubt investors consider any stock invincible, yet that did not keep some from being valued that way (or darn close to it). It is not surprising we saw some volatility as the market rethinks many of these names.

Much of this year’s rush into software and tech has been due to the belief these products would be least affected by COVID-19 due to their mission-critical nature. While that makes perfect sense, it does appear we have reached a point where even these expenses are being scrutinized. It is important to remember though all things are relative, and even after “weak” reports these remain some of the best businesses around.

As we exit earnings, I feel the underlying theses for most of my companies remain very much intact. At the same time, enough customers are either pausing or consolidating operations to pressure growth. Consequently, we have seen some multiples contract as stocks priced for great results only came in at good. I am OK with that. History has shown multiples for growth stocks always ebb and flow. Fortunately, history also shows the best companies tend to win big in the end. So, that is where I will keep my focus as long as the stories continue to hold.

2020 Results:

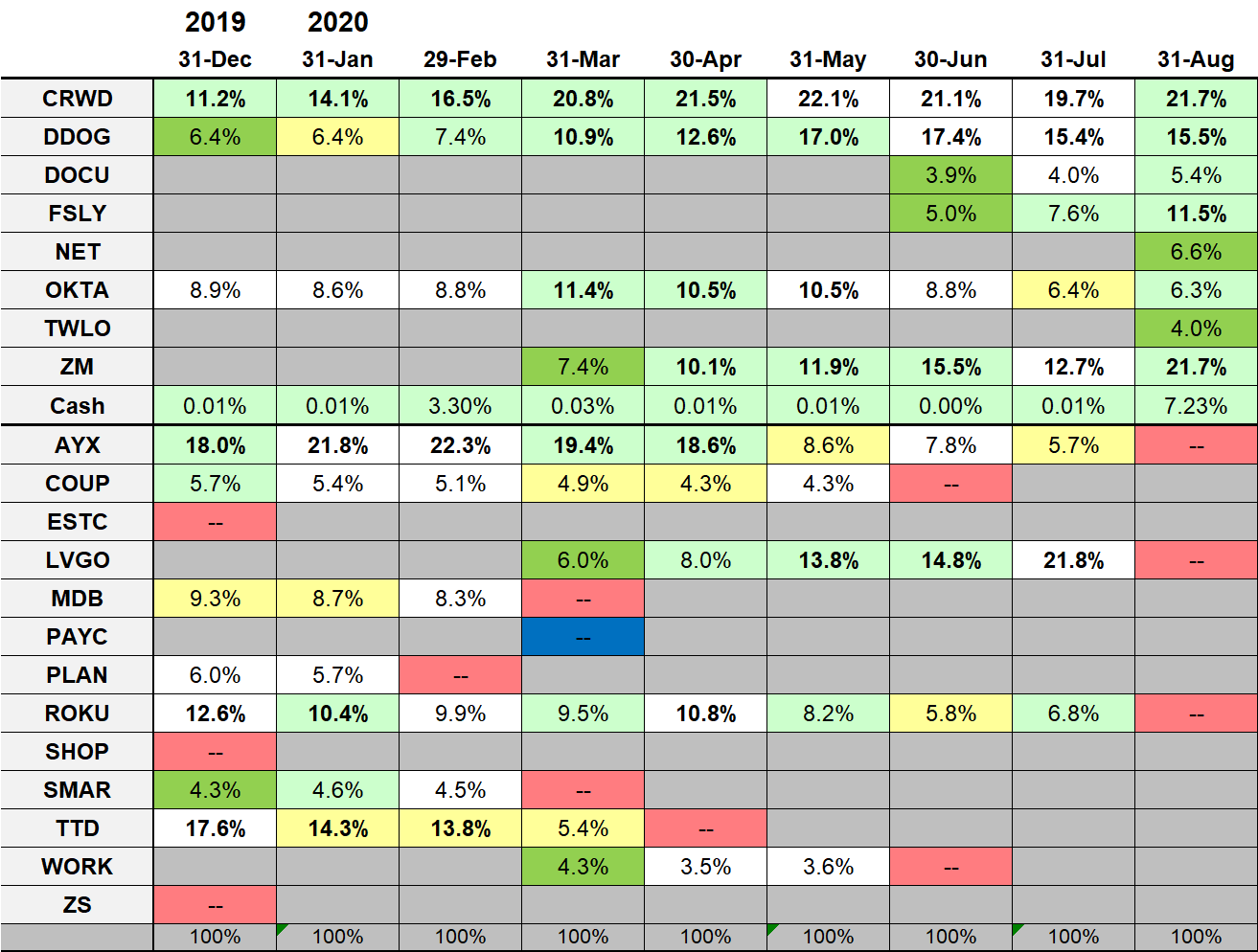

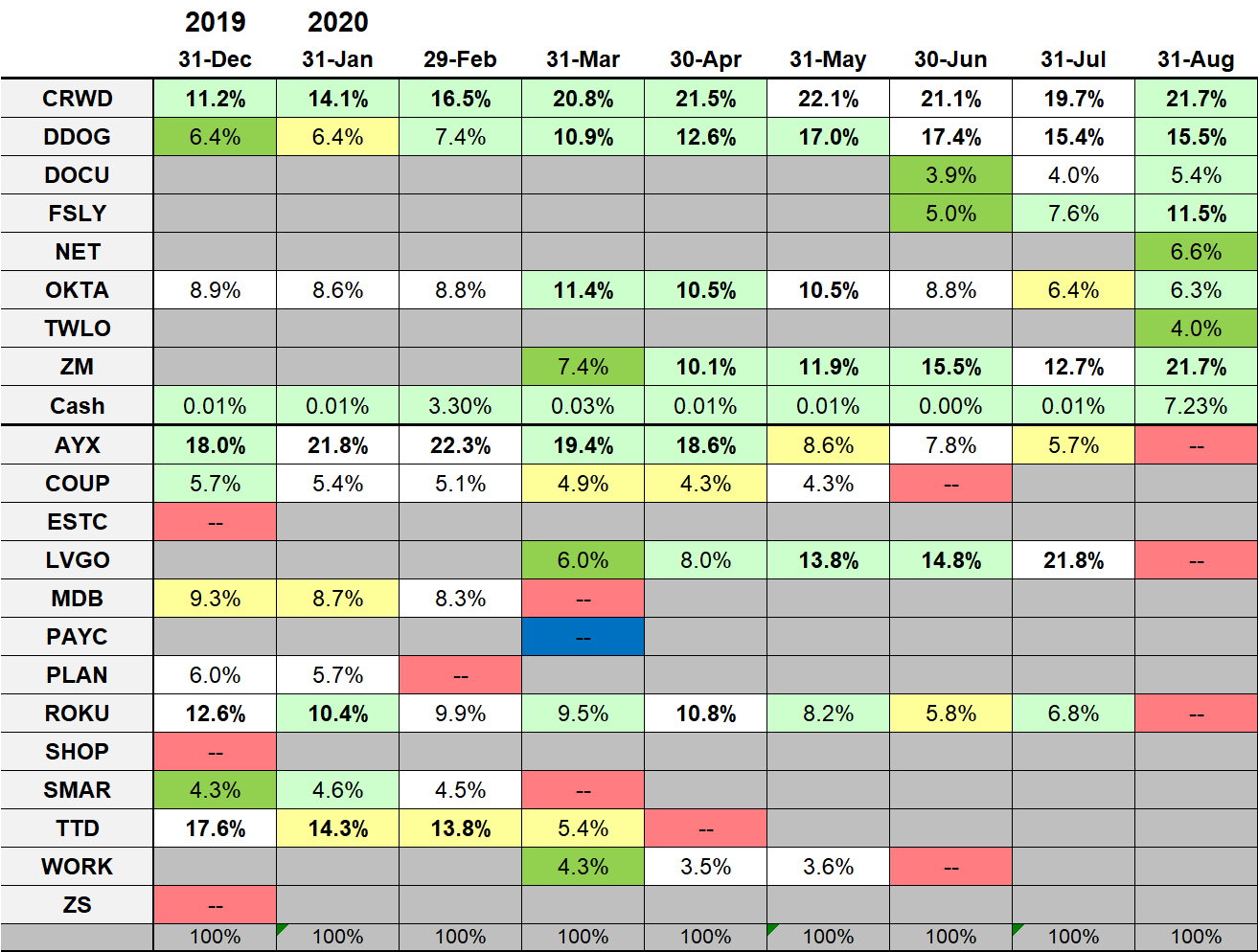

August Portfolio and Results:

2020 Monthly Allocations:

Key:

darker green - started during month

lighter green - added during month

yellow - trimmed during month

blue - bought and sold during month

red - position exits

positions >10% in bold

Past recaps:

December 2019 (contains external links to all 2019 monthly reports)

Stock Comments:

August turned wild right out of the chute. The fun started August 5 when Livongo was shockingly acquired by Teladoc on the same day Fastly and Roku reported. That was immediately followed by Alteryx and Datadog results on 8/6. It was an avalanche of information in ~36 hours on roughly 60% of my portfolio. After digging through it all I determined AYX and ROKU no longer met my criteria for holding. I also decided I did not want to own TDOC. Despite the stock hits to DDOG and FSLY, I felt the companies performed fine and had no problem keeping the shares.

The sudden events caused some portfolio upheaval and an almost 30% rush of cash. That put me in the fortuitous – i.e. lucky as hell – spot of having a boatload of dry powder when the market flashed deep red on 8/7 and continued to sag the following week. My first step was what I always do when allocating cash – test my maximum allocation for current names before reviewing my watch list. Peter Lynch once said, “The best stock to buy is the one you already own.” While not true every time, it is surprising how often that is indeed the case. So, my initial moves ended up increasing every position but OKTA. Only after I finished with cash remaining did I look outside and eventually add two new positions. I still have some cash to spend as we enter September but am content with where I stand. The hows, whats and whys can be found below.

AYX – It turns out Alteryx was not kidding around when it suggested this could be a rough quarter. Its headwinds have now become a full-on speedbump. Raw revenues once again shrunk sequentially, and growth has slowed from 76% to 43% to 17%. It does not appear things will improve any time soon with next quarter’s guide just 11% at the top end. To make matters worse, expenses as a percentage of revenues have spiked the last two quarters even as management tries to sharply curtail them. This has led to consecutive operating losses after ten straight quarters of profit. Meanwhile, net expansion has steadily slid from 132% to 130% to 128% to 126%. Alteryx’s 91.4% gross margins remain among the best around, but everything else is regrettably moving in the wrong direction.

The foreseeable future is not much better. Management says “uncertainty…will continue for some time” and projects “[based] on what we see today, we do not anticipate a material improvement in business conditions during 2020.” Not only are remote sales lagging, but management admits a “struggle to effectively onboard and enable some of our new hires particularly new sales reps learning our systems playbooks and new product offerings.” The CFO noted global go-to-market weakness and rattled off a list of sales metrics the company would continue to monitor “to inform us of how or if we continue to invest during the remainder of the year”. If?!? That does not sound good at all. I have always admired Dean Stoecker as a quality CEO. I also consider him one of the more knowledgeable and confident executives around, so the somber nature of his comments really stood out.

One concern I just can’t shake is AYX’s traditional pattern of lower Q1 revenues followed by acceleration through the year. Even management has noted it each of the last two years. This means COVID is drastically affecting what have traditionally been Alteryx’s strongest quarters. The timing means very tough comps the rest of 2020, which no doubt contribute to the low Q3/Q4 estimates. These difficult comps are compounded by accounting rules requiring Alteryx recognize roughly 40% of new contracts as revenue up front. I do not have to be an accountant to know that kind of frontloaded math can cause a severe drop off if business slows. That appears to be exactly what is happening.

I still like Alteryx’s business and have faith in its long-term value to customers. The problem is AYX’s short-term value does not seem to be a client priority right now. According to the CEO, “conversations with customers indicated that many thought to leverage their existing investments rather than undertake large new projects.” While Alteryx has responded by offering shorter contracts to entice customers, it is clear the sales cycle has become much tougher. I do not view Alteryx’s long-term thesis as broken. I do however see it as being on the injured list until COVID dissipates and AYX’s customer base can return to more normal operations.

In broad terms Alteryx hit the double whammy of an unprecedented macro slowdown and accounting rules that amplify the damage. That is a tough break for everyone involved. In my opinion the remainder of 2020 looks like treading water at best. A possible silver lining is the difficult second half should lead to much easier comps in 2021 assuming business returns even partially to its prior trend. I do believe Alteryx manages this period, but the present challenges make riding it out unappealing. For that reason, I sold my shares. I held off for a few days after earnings when I should have just swallowed hard and taken the full tax hit as soon as I got queasy. Lesson learned since I cost myself some profit. I would anticipate being back in Alteryx sometime during 2021.

CRWD – Alrighty then. Our next SaaS contender is about to step into the earnings ring. Just how well did CrowdStrike’s business hold up this quarter? I have no idea, but we are about to find out. I calmly await CRWD’s September 2 report.

DDOG – Datadog’s August 6 earnings had been circled on my calendar for quite some time. The good news is the company delivered a solid beat and raise. The bad news is the outperformance fell short of what the market was used to or expecting. Revenue growth of 68% was slightly above the top end guide while gross profit grew 79%. Gross margins held steady sequentially at 80% and improved from 75% in 2Q19. Customers with $100K+ ARR grew 71% and now stand at a total of 1,015. So, the headline business appears to be in fine shape.

Digging deeper, the secondary numbers suggest the same. Growth continues to outpace expenses, and DDOG remains solidly profitable. The company posted positive operating (11.0%), net (12.5%), and free cash flow (13.3%) margins for the fourth consecutive quarter. 68% of customers now use 2+ products vs 40% in 2Q19. In addition, 75% of new customers onboarded at 2+ suggesting this number should drift higher as we go. The number of customers using 4+ offerings was 15% vs 0% last year. Net retention was 130%+ for the 12th consecutive quarter even as management noted some macro pressure and slight churn. Something to watch maybe, but not a concern. If nothing else Datadog appears to be keeping customers happy.

Management’s comments expressed confidence, and DDOG continues to build for the future. The company furthered its FedRAMP approval and is now fully available in the FedRAMP marketplace. In conjunction with earnings DDOG announced the acquisition of Undefined Labs, “a testing and observability company for developer workflows”. According to the release, the acquired tech allows developers to monitor and assess software performance much earlier in the development cycle. Having a monitoring tool in the pre-production stage should greatly help clients with speed to market. It should also allow DDOG to engage customers much earlier in the product lifecycle. While I might not understand all the tech behind it, the concept makes perfect sense in our rapidly evolving digital world.

While no firm can entirely avoid COVID’s macro effects, Datadog is in a reasonable spot even when acknowledging many clients are currently looking to save rather than spend. DDOG is still growing, continues to invest and most importantly keeps on innovating. Following earnings it launched a marketplace where partners can develop and sell applications built on Datadog’s products. The company also released add-on offerings for code performance, error tracking, incident management, and compliance monitoring. Whatever issues DDOG might have, standing still is not one of them.

The market expected big things from DDOG this quarter and pushed shares close to all-time highs into earnings. It quickly changed its mind post-release and clubbed the shares down 20%+. I understand the market’s desire for a safe port in the ever-lengthening COVID storm, but I thought the selloff was overdone. Everything I see in Datadog’s numbers and news suggests its thesis continues to be one of the better ones around. I gladly used the pullback to make several adds, including shares under $78. I see no reason why Datadog shouldn’t continue as one of my top positions.

DOCU – DocuSign just might be my quietest three-month 50%+ gain ever. Its business is more slow-and-steady than sexy, but DOCU has really benefited from the need to conduct business remotely. This has not only helped its flagship eSignature line but also increased exposure for its newer Contract Lifecycle Management (CLM) platform. I saw several promising trends in DOCU’s performance when I opened this position in June. We will see if any came to fruition when the company reports September 3.

FSLY – What a bizarre stretch for Fastly. The stock inexplicably rose nearly 50% over five trading days into August 5 earnings before just as inexplicably “crashing” 30%+ after the report to end up roughly where it sat all of nine days before. Granted this is not Hertz or Kodak level craziness, but it certainly was strange. Welcome to the 2020 stock market, y’all.

The report itself was a solid beat and raise which included the first positive EBITDA in company history. It also included the largest quarterly customer increase since IPO. Revenue growth jumped sequentially from 38% to 62% with a guide suggesting at least mid-50’s in Q3. Gross profit spiked 79% YOY and net expansion ticked to 137% from 133% last quarter. Expenses continue to shrink and came in at a record low 59.2% of revenues. Gross margins bumped to 61.7% vs 57.6% last quarter and 55.6% in 2Q19. Management reiterated margins will continue improving as the company scales. The record customer increase brings the total to 1,951, and the resulting 20% YoY growth is the largest on record as well. The surge in customers and usage produced an EBITDA margin of 8.8% with positive net and operating income as well. Next quarter’s guide also suggests profitability, and management felt comfortable enough to raise FY revenue projections to $300M. All in all, very encouraging results.

The conference call backed up the positive numbers. Management sees a wide range of interest and believes COVID has “permanently accelerated the need for businesses to focus on digital transformation”. Fastly remains on track with its Compute@Edge offering and expects further availability throughout the year. The company is also investing heavily in security to ensure working at the edge is safe and effective. Management says customers no longer want to deliver content without embedded security. Based on this feedback, FSLY is valuing “security as an equal consideration to performance and speed”. The CEO considers security an underrated strength and credits it for wins in education, e-commerce and financial services.

Fastly doubled down on this security push last week by acquiring Signal Sciences for $775M in cash and stock. The acquired technology will immediately help power a new Secure@Edge security product. According to the investor presentation, Signal Sciences brings a preexisting stable of 60+ enterprise customers, 70% of which will be new to Fastly. It also adds $28M in immediate ARR and 85%+ gross margins. So, this deal quickly expands Fastly’s security footprint while also being immediately accretive to its existing business. Well played, sir.

Notwithstanding the momentum above, there are two things I will be monitoring going forward. First is the organic growth in enterprise customers (defined as those spending $100K+ in a twelve-month period). Those customers account for 88% of FSLY’s revenues yet grew by only seven last quarter to 304. Management addressed the low add by stating they are happy with the amount of “new enterprise customers along with customers who grew into the category”. However, the net total was lessened by some COVID-impacted customers who fell below the $100K threshold. The good news is remaining enterprise customers seem extremely satisfied as average spend per customer increased QoQ to $716K from $642K. The Signal Science buy should obviously help both the raw numbers and potential upsells. Still, I will be watching how the enterprise numbers trend the next couple quarters at least.

The second item is the future of Fastly’s relationship with TikTok now that the latter is in the crosshairs of the US government. In the six months ending 6/30, TikTok represented ~12% of FSLY’s revenue with less than 50% of that in the US. While ~6% total is not an irreplaceable amount, any adjustment or ban of TikTok would have a negative impact. It is hard to see TikTok disappearing completely from the US landscape given its popularity and success, but this wall of worry is likely to remain until the issue is resolved.

Overall, Fastly’s business seems very strong. To date the company has had no problem scaling increased usage into an improved bottom line. It keeps innovating and sees efficiencies that should reduce computing requirements, increase capacity, and “ultimately increase the amount of revenue per server”. Management remains “confident in the demand for our mission-critical services and the continued momentum of our business for the remainder of 2020 and the years to come.” As a shareholder, that is what I like to hear.

I was pleased enough with the report to add some afterhours and then more as Fastly drifted over the next couple of weeks. I also purchased a tiny bit after the acquisition. The stock almost certainly got ahead of itself on the hype before earnings, but I believe the underlying business is doing just fine. Sometimes the market prices in “great” then overreacts when it only gets “very good”. I think that is what happened with Fastly and was glad to add shares. Time will tell if I made the right call.

LVGO – A huge July rocketed Livongo from #4 all the way to my top portfolio spot. I thought my August writeup would simply celebrate another stellar quarter, which it most certainly was. However, this recap ended up spinning in an entirely different direction. There was major Livongo news August 5 when it was acquired by Teladoc. Like many shareholders, I was disappointed LVGO gave up on going it alone. I did not see the announcement until well into the day so had time to scan the details along with some initial market reactions. After reviewing everything I decided to sell my position in full. I have passed on TDOC twice previously and do not have interest in owning it now even as only 58% of the combined entity.

TDOC/LVGO exits this deal a much different company with a much more complicated story. As a standalone Livongo was the spunky little upstart making inroads. This new pairing immediately faces a bigger, more convoluted market. Could TDOC/LVGO disrupt medicine? Sure. Will the more entrenched bureaucracies of doctors, hospitals, insurance companies, regulators and politicians let it happen without wrangling for their piece of the action? Doubtful. Don’t get me wrong. I am all for patients having a better healthcare experience. However, I say that as a fairly experienced US consumer in a system that currently makes it virtually impossible to determine how much a treatment even costs. I do not see that changing any time soon regardless of how many newfound operational synergies TDOC/LVGO says it has.

I have previously encountered healthcare-related stocks where the oh-so-obvious benefits of the company’s service should logically win the day. My experience is it never happens quite as easily as you think if it even happens at all. That is why I was already paying extra close attention even as Livongo became my biggest holding. I fail to see how TDOC/LVGO avoids the same slog. Despite management’s cross-selling giddiness, I will hold my excitement at least until the acquisition goes through. In the meantime, I am perfectly content to step aside for a while and see how things develop.

I was not fortunate enough to exit LVGO at the top – you can’t time the market after all – but I have zero complaints with how this turned out. Despite owning it for just five months, Livongo leaves as my most profitable purchase ever on a total dollars basis, and it is not even close. My total position built from March through July gained 304% with my cheapest shares climbing 435%. That is insane, even if hindsight suggests the final surge was probably due to some undercurrents from the acquisition. Regardless, I will gladly take the minor inconvenience of an unexpected influx of ~22% cash for that type of return. I wish those who held the best of luck and sincerely hope Livongo and Teladoc continue to make the world a healthier place.

NET – Cloudflare earned a spot in my portfolio after what I thought was one of this season’s better reports as far as meeting expectations. NET posted a strong quarter with a solid beat and raise. Top line growth held steady from Q1 at 48% with a Q3 guide suggesting something mid-40’s. Total customers grew 28% to 96,000. Meanwhile, customers spending $100K+ grew 56% to 637. US growth was 46% YoY and now accounts for 49% of total revenues. International was even better, growing 50% YoY for 51% of the revenue pie. Bottom line losses are steadily improving while cash flows continue to grind in the right direction. It was a good showing all the way around.

The call expressed a lot of confidence in the rest of 2020. Management happily noted several strong trends in the first month of Q3. COVID-related concession requests have tailed off. Collections have stabilized while the sales cycle remains at the low end of its historic range. NET’s virtual VPN product offered free through September now has 2,000+ companies enrolled. The CFO states “very little of this conversion is reflected in the forecast today”. While that conversion rate is still TBD, this could be a significant revenue driver in 2021.

In a challenging business environment, it makes sense to target mission-critical companies. I believe Cloudflare has earned a spot in that conversation. The company posted record hiring, continues to invest, and most importantly keeps executing its plan. Management says they have strong visibility into their pipeline and are comfortable they can maintain momentum even in these uncertain times. I must admit I found the confidence rather contagious and built up a healthy allocation during the month.

[Side Note: Cloudflare recently received some negative press when its Chief Security Officer was charged for non-disclosure of a 2016 hack while he was working at Uber. My initial take on management (particularly CEO Matthew Prince) has been positive, but this puts me on alert. I will hold the shares but be watching to see how this unfolds.]

OKTA – Okta was the only position I did not bump after my LVGO windfall. The decision was two-fold. First, the stock has always been pricey even though I believe its leadership and competitive position justifies some premium. Second, management’s clear reference to headwinds in last quarter’s call had me cautious heading into August 27 earnings. I decided to stand pat until I saw the results.

It turns out Okta had one of its usual metronomic quarters. It posted a strong beat with revenue of $200M and 43% growth. Subscription growth was 44% and 95% of total revenue. International revenue grew 47% and now accounts for 16.1% of Okta’s total. Enterprise business and total customer growth remain steady with limited COVID effects. Okta also crossed a milestone with over 100 customers now spending $1M+ in annual contract value (ACV). Net expansion held sequentially at 121% and improved YoY from 118%. Finally, remaining performance obligations hit a record $1.43B (+56% YoY) with $684.5M due within the next 12 months. In a nutshell, Okta continues to execute and is doing it at scale.

Digging into the secondary numbers, Okta’s increasing efficiency and leverage are really starting to find the bottom line. Total and subscription gross margin hit record highs of 78.9% and 82.8%, respectively. Expenses were lower than expected due to continued travel and office costs, but headcount increased 28% to ensure enough customer-facing teams to service clients. That is a smart investment in my book. Despite the relative lack of fanfare, it is worth noting this was also Okta’s first profitable quarter. It posted $6.5M in operating income (3.2% margin) and $9.9M in net income (4.9%). Free cash flow ($6.9M) was positive for the fourth consecutive quarter and 7 of the last 8. While the CFO stated not to expect “consistent profitability in the near term”, next quarter’s guide and the long-term trend makes it perfectly reasonable to assume Okta is not far away from turning over the profitability leaf for good. COVID headwinds or not, the core business is plugging right along.

Management’s call backed that sentiment in spades. First, Okta treated investors to its first-ever video earnings call (powered by Zoom, of course!). CEO Todd McKinnon expressed considerable confidence in where Okta is headed. He stated customers are using the platform more than ever, including 16 billion unique logins in March-July (+70% YoY) and a one-day record of 145 million. I must say, that’s a whole lotta logins. McKinnon also noted increased traction in Okta’s newer customer identity products, which grew 72% YoY and now represent 24% of total ACV. The CFO was confident enough to raise the FY21 guide. TAM’s are always a bit inflated, but he estimated $30B for workforce identity and $25B for customer identity in response to an analyst question. That suggests Okta still has plenty of room to run.

In my opinion Okta is kinda what a rock-solid company is supposed to look like. It has excellent management that cares about its people and products. It consistently posts strong growth and gross margins while losses turn toward profits as the company scales. We have seen something similar in recent years with successful names like PAYC, VEEV and TTD. Okta appears to be following the same blueprint. I continue to like what I see and will be keeping Okta right where it is in my portfolio. I even added another 0.5% on the post-earnings dip.

ROKU – Last month I expressed some uncertainty surrounding Roku’s August 5 earnings. Unfortunately, for the second consecutive quarter Roku left me feeling lukewarm. Despite active accounts, player revenues and streaming hours all reaccelerating, monetization remains as elusive as ever while advertisers wait for COVID to pass. As many familiar with Roku know, player sales are not meant for profit but to increase the number of viewers on its platform. Platform fees and ad sales always have been and always will be the major drivers of Roku’s thesis. Unfortunately, the pandemic continues to heavily pressure both. Platform revenue growth tumbled from 73% to 46%. Not surprisingly, platform gross profit growth sank as well from 39% to 26%. Video ad impressions were up 50% YoY, which sounds impressive until you consider management has been loosely trumpeting this metric as “more than doubled” for several quarters. It is very likely just a large numbers slowdown, but it is hard to tell for sure since management does not break this out specifically. Regardless, it is clear the general woes in the advertising market continue.

Beyond the headlines, secondary metrics lagged as well. Platform gross margin was 57% and remains down sharply due to ad pressure and revenue mix. Platform revenue as a percentage of total decreased sequentially from 72.5% to 68.7%, which means Roku will almost certainly fall well short of its initial FY20 goal of 75% platform share. International efforts continue (as they should) but have yet to show any real traction. Even this quarter’s EBITDA beat was somewhat tainted since it was driven mostly by reduced expenses rather than business growth. Despite the continuing march of consumers toward streaming, turning additional viewers into bottom line success remains a struggle.

I still believe Roku has a bright future, but the ongoing uncertainty suggests its time might be further off than I thought. I don’t disagree with management’s comment we are “very early” in a global move to streaming. The problem is the ever-lengthening path to profits hints it might also be too early for Roku to create the business leverage I have been waiting for. Simply put, I feel other companies are executing better. Through my lens Roku’s numbers have barely supported the narrative the last couple of quarters. This quarter I feel they disconnected. With the drastic platform slowdown and a warning “it will be well into 2021 before TV ad investment recovers to pre-pandemic levels”, I decided my money is better off elsewhere. I could very well be back, but not until Roku proves it can better leverage its bottom line.

TWLO – Twilio rejoins my portfolio after a 9-month hiatus. I sold last October when I felt the company struggled to integrate the SendGrid acquisition and find traction with its Flex contact center product. To make matter worse, I thought the CEO played a little loose with the numbers in trying to explain it all. TWLO never fully left my radar though and now appears to have smoothed out most of the wrinkles.

I was already curious about this quarter’s report since it was the first apples-to-apples comparison including SendGrid. There were several things to like. Revenue growth was 46% with an expansion rate of 132%. That compares favorably to Q1’s 48% organic growth and 135% DBER. Next quarter’s guide again suggests revenue near the mid-40’s, so growth seems to be stabilizing at a healthy rate. Active customers reached 200,000 for the first time with YoY growth accelerating slightly to 24%. Expenses came in at a record-low 53.5% of revenues. The result was another slight profit, marking the second consecutive quarter of positive operating income and ninth for net income. Twilio is apparently finding its niche.

The call comments were positive, and management believes Twilio is well-positioned through the end of COVID and beyond. I was pleased to hear the discussion on Flex. As mentioned earlier, lagging adoption of Flex after being highly touted by management was a main factor in my October sale. Its popularity is now on the rise, especially as customer service agents work from home rather than crowded call centers. COVID has accelerated this move, and it is perfectly reasonable to think cost efficiencies will keep much of this model viable post-pandemic. Management described onboarding recent clients in as little as “a couple weeks”. Replacing legacy systems will take longer, but that does not change the fact Flex’s ease of use bodes well for the future.

A second highlight was the early traction in healthcare communications offerings. Twilio’s HIPAA compliance efforts have paid quick dividends as the need for remote healthcare has surged the last few months. As with remote call centers, it is reasonable to assume many benefits of the digital health model should remain post-COVID. This appears to be yet another vertical where Twilio has plenty of room to grow.

While I would no longer classify Twilio as hypergrowth, I do believe it has regained some mojo as an attractive growth option. The business remains strong, and its usage-based model fits the times. The product line keeps expanding, including a foray into embedded video. Finally, it is worth noting increased usage for US elections should be a nice second-half buffer as new initiatives hopefully continue to take root. Twilio has a lot going for it right now.

Addressing my other issue, did CEO Jeff Lawson previously move the goalposts by highlighting post-acquisition numbers that did not quite represent TWLO’s true performance? I believe so, and that admittedly rubbed me the wrong way. Exaggerations aside though, Lawson deserves credit as a passionate leader who genuinely believes his company can help developers build a better communications experience. That is encouraging, and I am less concerned with future comps now that TWLO has lapped the SendGrid acquisition and the numbers are more straightforward.

One of the many side effects of COVID has been businesses around the world scrambling to improve customer engagement on a digital scale. That is right in Twilio’s wheelhouse, especially considering the flexibility and customizable nature of its products. Management sees broad opportunity and “traction in healthcare, education, financial services, retail contactless delivery and e-commerce”. In fact, both the CEO and CFO used the phrase “Twilio is built for this” on the call. I find that argument valid enough to reopen a position and follow along for a while.

ZM – We all knew Zoom’s August 31 numbers would be big. The only question was just how big. Well, it turns out they were freakin’ ginormous. At some point you simply run out of superlatives for what Zoom is doing. I seriously doubt any company ever has posted these kinds of numbers at this kind of scale:

I could break it down further but take my word for it: ALL the numbers are like this. Revenues, customers, expense ratios, profit margins…no matter how ridiculous the estimate, Zoom obliterated it for the second quarter in a row. It has been incredible to watch.

CEO Eric Yuan says Zoom is helping the world “actively [redefine] and [embrace] new approaches to support a future of working anywhere, learning anywhere, and connecting anywhere.” Book clubs, poker nights, birthdays, weddings, business meetings, telehealth, education, government hearings, legal proceedings – it doesn’t matter. All are experimenting online, and I believe more formats than we think will stick post-COVID. Zoom is clearly leading as the platform of choice in this budding virtual world.

What is most amazing to me is just how big Zoom’s total market could eventually get. As highlighted above, the Americas grew 288% this quarter while the rest of the world grew 629%(!!!!). With international revenues still just 31% of Zoom’s total, that means the larger untapped market is growing more than twice as fast off an already sizable base. Even better, these rates accelerated from Q1 when the Americas grew 150% while international grew 246% and accounted for roughly 25% of revenue. Just take another look at those figures. The international opportunity is enormous, and the exponential growth suggests to me Zoom’s phenomenal performance will not end any time soon.

As for the stock, my position increased significantly in August. First, Zoom received a larger portion of my LVGO proceeds than any other holdover. Second, the stock had a backloaded +28.0% month from which a lot of those new shares benefited. I firmly believe ZM is as well-positioned as any company in the market to continue thriving both during and after COVID. This fantastic report only strengthens that belief. The late August rise moved Zoom ahead of CrowdStrike for my #1 spot at 21.73% to 21.69%. The strong post-earnings pop lengthened the lead heading into September. I fully expect these two to keep jockeying for position at the top of my portfolio for the rest of 2020.

My current watch list…

…in rough order is SHOP, COUP, TTD, ROKU and MDB. All are good names, but none immediately trips my trigger quite enough to grab any of my remaining cash. I will wait for September’s final few earnings reports before deciding what to do.

Also, I dug around on Sea Limited but found it too complicated. It is basically three businesses in one: gaming (big revenues with big profits), e-commerce (big revenues with big losses) and digital payments (tiny revenues with big losses). It looks like SE is using its gaming profits to fund the other two. If I have it right, the company might also stop issuing adjusted revenues going forward which reworks all the numbers. I somewhat like the story but cannot see how I would get comfortable with anything more than a tiny speculative position. Tiny speculative positions are not really my thing, so I am a pass for now.

And there you have it.

What a rollercoaster month. My portfolio’s insane run from the March lows extended into the first few days of August. I hit 120.3% YTD on 8/4 before the wheels temporarily fell off. It started with a one-day 9%+ drop on 8/7 followed by a steady drift downward the next week. Fortunately, I had plenty of new cash to throw at the dip. I ended up seeing an almost 20% drawdown over the next 10 days before somehow clawing back to finish at a new all-time high. I will gladly take that outcome after the mid-August swoon.

Those who have followed along for a while know I prefer being fully invested. Frankly, the glut of LVGO cash in early August caught me totally off guard. I gave it my best effort but was not able to comfortably reallocate it all by the end of the month. I know there’s no rush, but I do intend to put it back into play in September. The plan is to let my last few names report so I have a clear view of the landscape, then decide where to spend the cash from there.

As summer draws to a close, I can only say this has been quite a year. COVID-19 is remaking our entire planet, and many of the changes will be permanent. For one, the steady march online is now an all-out sprint for areas like work, communication, entertainment, and commerce. The companies best facilitating these moves have seen huge success, and several will lead the way post-virus as well. As this excellent article by Morgan Housel illustrates, many of history’s most innovative periods occur during our most distressing times. It would sure seem 2020 qualifies. Housel observes that mankind tends to produce amazing solutions when faced with seemingly unsolvable problems. Here is hoping that trend continues with COVID-19, and we quickly get to a better place on the other side.

Thanks for reading, and I hope everyone has a great September. Oh, and don’t forget to keep washing your hands and wearing your mask.

Hi Stocknovice,

As I review the results and reports coming in for the month of Sept, I am impressed with the apparent continued growth of DOCU, which I was just reminded of when I had several transactions to complete. It was as smooth as silk. I also took note of Paul Bryants observations this evening on Saul's discussion board.

I hold DOCU . It is about 7% of my current portfolio. I have a bit of cash but I can't decide whether to sink more into DOCU or try to augment my FSLY now at 12%. Decisions decisions.

I haven't seen or heard any reasons to lighten up on either LVGO or SE but I am ready to cut bait at a moments notice if necessary. There was a recent report on a survey of online shoppers in Indonesia who prefer Shopee to other options by a wide margin. It was also reported that the number of ecommerce platforms in SE Asia is much depleted by competitive pressures. Meanwhile Shopee thrives.

Paul referred to your early Sept post which I reread. That motivated me to communicate here. Do you have further thoughts on any of the aforementioned issues. I would be most interested in how positive you are now regarding DOCU.

For my part I have a growing conviction in DOCU because they are expanding their product offerings and because its one of those services that everyone will need to use.

cheers

arnie

Hello,

And thank you for your blog! It is very good example how anyone that takes investing seriously, has to proceed. I also must start taking such notes, but yours look like a fairy tale - so well written and easy to read!!!

Let me ask you a question with an example.

Let's take two companies - CRWD and PTON. Both of them reported earnings this month. CRWD's stock went down, but PTON went up after-market, although both had amazing results. I do not discuss the reasons why this happened.

My question is - when you suspect good results and have some amount willing to add to the position, do yoу spend half of it before the earnings and the other half after?

I know that there isn't one-fits-all answer, but I'm curious what's your oppinion.

Cheers and thank you.